There was a time, seemingly not long ago, when Joe Royal felt he should only use his debit card for larger purchases.

These days, however, the 44-year-old from Indiana has no qualms about swiping his card to pay for a $1.49 pack of chewing gum at a 7-Eleven store. And, although the store owner has to share a percentage of that sale with the credit card processor, cashiers do not seem to mind, possibly because they have now grown so used to the process.

Will contactless payment help phase out cash?

Royal can go days without seeing any cash at all. His paycheck is direct-deposited into his checking account. He pays for gasoline at the pump. He pays highway tolls with a device mounted on his windshield that pulls money from his checking account each month. A website feeds his children’s school lunch money cards from his checking account when the balance reaches the minimum amount that he has chosen. He pays his bills online.

His credit union gives him a cash rebate when he uses his debit card as a credit card, giving him more incentive to use the card wherever possible.

Of course, Royal is far from alone. From America to Zimbabwe, the world is slowly but steadily changing to a cashless society. We do not even need a card any more, thanks to payment methods from Apple, Google and Microsoft that let us simply swipe our phone across a sensor.

Royal says he never intentionally stopped using cash. “I just realized one day that it had just kind of happened,” he says.

Royal still has the freedom to choose whether he wants to use cash, but many observers fear that this will not always be the case. Governments and mega-corporations, such as MasterCard, are working hard to abolish cash. MasterCard is pushing the War on Cash agenda with its “Cashless Journey” project, which deploys a website and public relations campaign to spread the message that cash is inconvenient and invites theft and tax evasion. It urges “government focus and technological innovation” to hasten the death of cash.

Cashless payment methods can be convenient but a growing number of experts are urging governments to always preserve cash as an option because of its utility for small transactions and its use by poor people who lack access to financial institutions.

It is not hard to find examples of nations trying to pave the way toward the extinction of cash. Last year, the government of Denmark announced a proposal to exempt some types of retailers from the requirement that they accept cash, arguing that it costs too much to process and poses unnecessary security risks.

In 2013, Canada stopped circulating the penny, a move some fear is a precursor to phasing out cash.

Governments claim that they are waging their War on Cash in pursuit of greater efficiency but critics suspect a darker motive. In a world of strictly digital transactions, the state will know exactly how each citizen spends his or her money. Harnessing that information will give governments an even greater power than they already exercise.

While these trends are unsettling, there is reason for hope. Like so many futile efforts before – think the wars on drugs, terrorism and prostitution – the War on Cash is likely to be destined to fail.

People are already so cynical about government and their political leaders that it is difficult to imagine that they will easily give up their right to use cash.

Donald Trump has been a controversial and scandalous figure ever since his announcement to join the race for the Republican nomination and subsequently run for the presidential election back in June 2015.

In his presidential announcement speech, he has revealed a hostility towards Mexico and China, referring to undocumented Mexican immigrants as rapists and drug dealers, and boasting about beating China in business deals “all the time”.

Regrettably, this wasn’t the end of his controversial dialog. In summary, he called for a prohibition on all Muslims entering the United States; advocated killing the families of jihadist terrorists; described on China and Japan as “currency manipulators”; and repeated a negative narrative that American soldiers in the Philippines in the early 1900’s dipped their ammunition in pigs’ blood before executing Muslim terrorists.

This is by no means an exhaustive list. In a recent rally he said that he would like to punch a protester in the face and, even more recently, warming to his theme, he upset the already besieged people of Belgium, many of whom had lost their families and friends, by describing its capital, Brussels as “a hellhole”.

Despite the controversy and lacklustre support in the early stages of the Republican nomination race, Donald Trump has gained significant momentum and looks increasingly likely to secure the Republican nomination.

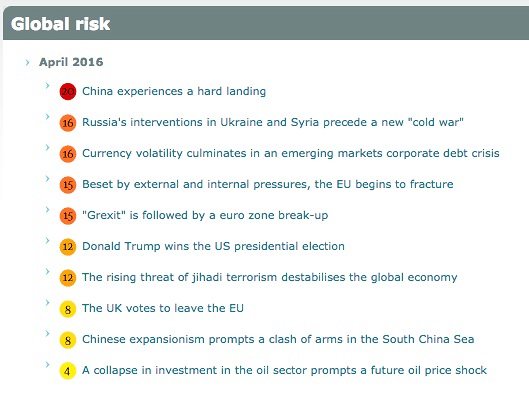

Many governments, corporations and influential individuals around the world have expressed grave concerns about Mr. Trump’s destabilising influence and potential presidency. Specifically, the Economist Intelligence Unit (EIU), a renowned global economic and geopolitical analysis firm, placed Donald Trump’s presidency sixth on their latest list of global threats, on a par with the rising threat of jihadi terrorism.

Economist Intelligence Unit’s latest list of global risks

Donald Trump has been extremely provocative and far from conservative on many of the social and economic issues, which has raised concerns globally. According to the latest EIU report, “his militaristic tendencies and controversial remarks towards the Middle East would be a potent recruitment tool for jihadi groups, increasing their threat both within the region and beyond”.

Illustrative of this, Donald Trump was featured in the propaganda video praising ISIS’s attack on Brussels and calling for more killings in Europe. Robert Powell, global risk briefing manager at EIU, also adds that “One of [Trump’s] extreme positions has been to invade Syria to wipe out ISIS”, citing estimates that a year-long incursion into Syria of 20,000-30,000 U.S. troops could cost $25 billion (£17.6 billion).

Moreover, Trump has advocated plans to seize Syria’s oil fields and refineries, which finance ISIS, and then selling the oil to pay for a U.S. military campaign. However, according to Powell, at current oil prices, this strategy would only net about $500 million (£351 million), at most.

Donald Trump, throughout his campaign, has failed to set forth a comprehensive and clear-cut domestic or foreign policy. The only unambiguous policy Mr. Trump advanced was the construction of a wall along the United States’ southern border, paid for by Mexico which makes no practical sense.

It is unclear as to how he would react and govern the country if faced with serious issues such as disputes in the South China Sea, a terrorist attack on American soil or another financial crisis.

Moreover, the statements made by the President of the United States can have serious economic consequences, both domestically and internationally. Considering the extent of the market’s reaction to only two or three words from the Federal Reserve Chairman, this may not prove to be an overstatement of the impact that an ill-chosen statement by Mr Trump, as President of the USA, might have and the blunt way of speaking that has made him so popular among Republican voter could be disastrous if he is in the white House.

The World’s largest insurance market is challenged by continued pressure on pricing and low investment returns

Lloyd’s of London insurance market has posted a 30% drop in profit in its financial year 2015.

The specialist insurer’s market announced last week a profit of £2.1 billion ($2.98 billion) for 2015, representing a serious drop from the £3.0 billion generated in 2014.

John Nelson, Chairman of Lloyd’s, said “In a market undeniably tougher than seen for many years, in 2015 we have had to demonstrate our determination, innovative thinking and ability to adapt and take action.

The significant pressure on premium rates and exceptionally low investment returns have, naturally, had an impact on our results. Low interest rates and low investment returns generally in the capital markets continue to attract additional capital into the sector.“

More than 80 syndicates underwrite insurance at Lloyd’s, covering all classes of business. Together they interact with thousands of brokers and agents daily to create insurance solutions for businesses in 220 countries and territories around the world. Lloyd’s insures the majority of FTSE and Dow Jones industrial average companies.

The annual report announcement contained some positive elements such as the six per cent improvement in gross written premiums to £26.7 billion ($38.4 billion) from the £25.3 billion in 2014. In addition to the seven per cent increase in the capital assets to £25.1 billion ($36.1 billion)

Despite the drop in profits, Lloyd’s remains committed to driving forward with its Vision 2025 plan, which includes the expansion into new markets such as Dubai, China, Turkey, India and South America and many others.

President Obama unveiled a set of changes to the Unemployment Insurance (UI) system on Saturday aimed at providing more security for out of work Americans and encouraging them to re-join the workforce.

The President’s proposals focus on three major elements: Protecting workers with wage insurance, strengthening unemployment insurance and making it easier for workers to retool and retrain.

The aim of the proposals is to ensure Americans can rely on UI to provide basic support during difficult times by expanding coverage and ensuring states have the resources to provide benefits

The president’s proposal would require states to provide wage insurance to workers who lose their jobs and find new employment at lower pay. The insurance would replace half of the lost income, up to $10,000 over two years. It would be available to workers who were with their prior employer for three years and make less than $50,000 in their new job.

The plan would also address holes in the UI system by expanding coverage to part-time, low-income, intermittent workers and workers who leave work for compelling family reasons. It would also ensure that states provide at minimum 26 weeks of coverage.

Furthermore, companies will be encouraged to avoid layoffs but instead opt to work-sharing schemes.

More detail on these proposals will be described further in the Obama’s next month budget

If you haven’t already seen it, you should definitely check it out!

Myke Tyson, the former boxing champion, took a nasty fall when trying to ride his daughter’s hoverboard. The heavyweight champion then posted a video of the accident in his twitter account. The funny home video went viral on social media and picked up over 48,000 retweets.

The video shows Mike Tyson taking a couple of spins on the self-balancing two–wheeled board in what seems to be his living room. Feeling the growing confidence in controlling the gadget, he claps his hands for joy and then attempts to move forward before losing his footing and falling flat on his back with a loud thud.

Tyson’s tweet suggests that he took the fall in a good spirit, however and unfortunately there were many cases in which people hurt themselves very badly.

When did they get so popular

A quick search into Google Trends shows that the rise in popularity of these fancy gadgets is quite recent

Interest over time. Web Search. Worldwide, 2009 - present.

Google Trends – Web Search interest hoverboard – Worldwide, Jan 2009 – Jan 2016

Most people treated the hoverboard as an expensive gadget for the rich and the famous, but recently in social media many celebrities posted photos and videos riding and enjoying them.

Chinese companies banked on the popularity and helped fuel the global craze by making cheaper versions thus reducing the price it costs to acquire one, especially for christmas as a present.

The speed and the lack of safety standards to manufacture the hoverboards by the Chinese companies has given it bad publicity – they keep exploding

Over the past several months, local fire departments around the world have reported incidents involving hoverboards catching fire.

In the UK, the London Fire Brigade (LFB) issued ‘hoverboard safety’ warnings urging people to be careful and to not to leave their devices unattended when charging. The reason is that LFB’s been called out several times last October 2015 because of fire starting from these devices in their houses.

In Louisiana (US), a couple of days just before Thanksgiving Jessica Horne bought her 12’s year old son one of those devices. But just one day after using it, Jessica’s son was charging the battery using the charger that came with the hoverboard. A moment later their house was destroyed. She said she saw flames shooting from both ends.

The reasons why so many hoverboards are catching fire are due to the lithium ion batteries in these devices reportedly catching fire. Lithium batteries are commonly used in re-chargeable devices because of their long life and ability to provide high currents very quickly. However, a too rapid discharge of a lithium battery can result in overheating and causing the device to catch fire and even explode.

In the UK, the government is already cracking down on hoverboards. The UK National Trading Standards body has now seized and reportedly destroyed 32,000 hoverboards – the vast majority of the 38,800 devices that the organisation has been tracking since it started investigating the devices in October. Furthermore, it is now illegal to ride one on public roads or pavements as the potential to cause damage to others is greatly increased.

A high profile example is the Jamaican sprinter, Usain Bolt, who was knocked over by a hapless cameraman on a segway moments after winning the 200m world title at the World Athletics Championship last summer in Beijing, China.

Like with any new technology, it’s very difficult to say whether it’s a temporary phenomenon or it is here to stay. One thing for sure it’s causing a lot of harm to the early adopters and already the technology is forcing to government and companies to work in tandem to ensure the safety and security of all party involved.

Austrian World Cup slalom skier Marcel Hirscher had a lucky escape after he narrowly avoided being hit by a local television drone.

The skier was taking part in the Alpine Skiing World Cup slalom race in Madonna di Campiglio in Italy when the drone-mounted camera came crashing few centimeters past him.

Despite the incident, the defending champion managed to come second in the competition just behind the Norwegian Henrik Kristoffersen.

The International Ski Federation released a statement on its website apologising for the unfortunate accident.

New York based startup Lemonade secured around $13 million in funding from Sequoia Capital & Aleph last week to launch the world’s first peer-to-peer insurance company in the United States.

Lemonade was founded by veteran tech entrepreneurs Daniel Schreiber and Shai Wininger. Schreiber’s experience spans startups to Fortune 500 and most recently being the President of Powermat Technologies (consumer electronics). Wininger became prominent when he co-founded the marketplace for gigs (small jobs) Fiverr.com

The peer-to-peer concept was popularised in the early days of the Internet by the file sharing systems like Napster. From then, it propagated to other part of the economy, which gave rise to companies like Uber, the car sharing app, and Airbnb, the home renting service.

The implications of the peer-to-peer economy, also referred as the ‘sharing economy’, activity have been greatly debated in the media and the business world because it has succeeded in disrupting a number of business models.

However, one of the industry that hasn’t been disrupted yet is the insurance industry. The regulatory regime complexities, huge amounts of capital to start with and resistance to change steeped within the industry has made it resist a little bit longer.

It’s the not the first time that the industry was confronted to new disruptors. For the past five years, a number of startups in different part of the world have tried to challenge the multi-billion dollar industry.

In Germany, Friendsurance started on the premise to offer a platform that allows people to form small groups of policyholders who then would receive a cashback bonus at the end of their policy if they don’t make a claim, as show in diagram below

Another startup based in China is making a name for itself, Tongjubao, the peer-to-peer insurance innovator takes on community social risks (divorce, career disruption) by pooling the risks via its collaborative risk sharing platform.

So far, most of the innovations embarked on were challenging the broking sector within the industry as most them allow customers to form groups and then simply get cash back.

Lemonade is taking on a bigger undertaking because the company has applied to be a licensed carrier, which means that it can underwrite and offer policies itself.

Wininger, President and CTO, said “We’re challenging the way insurance companies work, with a peer-to-peer business model fueled by self-serve technology,”

“We are building an insurance company fully vertically integrated from the ground up to rethink some of the building blocks of the industry,” says Schreiber

The insurance industry is rigid with because all the different laws and regulations and this makes it a good target for disruption.

“It is very unusual for a company to receive $13 million in an initial round of funding,” said Haim Sadger, Partner at Sequoia Capital. “But it is rarer still to find such accomplished founders tackling such a sizable industry with such a compelling solution.”

We’re betting Lemonade will transform the insurance landscape beyond recognition.

It is one to watch.”

Chubb, the global US insurer, has revamped its home and motor insurance offerings to include cyberbullying coverage to private clients policyholders, after feedback from brokers.

Policyholders who become victims of cyberbullying will be able to claim up to £50,000 towards professional support, lost income and temporary relocation costs.

The additional cover which comes under the home policy will provide not only the policyholder but also their family members support if online harassment causes them to miss work, school or college

Cyberbullying is defined by the insurer as “three or more acts by the same person or group to harass, threaten or intimidate a customer”

The policy changes came into effect last month for new business and will be made available for renewals from the 1st January 2016.

The new, improved and amended home and motor covers introduced within the company is a response to an extensive research to establish how to further enhance the quality of its products and services.

The research was conducted by YouGov in June to August 2014 on behalf of Chubb through a survey of brokers and UK and Ireland target consumers. The research revealed several areas where policyholders’ offerings could be made more competitive by including new threats covers.

Tara Parchment, UK and Ireland Private Clients Manager, said: “We’ve listened to the needs of our brokers and their clients, having engaged YouGov to undertake our biggest – ever research project. We learned a lot about the changing environment that we work in – clients want ever – faster service and brokers wanted us to create more innovative, differentiating covers.”

Ms Parchment added: “We are very proud about our new offering, which represents another Chubb milestone in bringing innovative covers and added – value services to the private clients market. We wanted our policies to reflect the changing nature of the risks that policyholders may face, often against themselves rather than their possessions. Consequently, we have introduced cyber – bullying, student fees and assault cover as standard.”

The government of Gibraltar has set up a new Protected Cell Company (PCC) category specifically designed for its insurance linked securities (ILS) market.

The new company to be know as SPV (Special Purpose Vehicles) PCC will be under the Gibraltar’s Insurance Companies Regulations 2009.

Following in the footsteps of other offshore jurisdictions such as Guernsey, Cayman Islands and Bermuda, Gibraltar hopes to attract ILS fund managers writing collateralised reinsurance business.

Albert Isola, Gibraltar’s Minister of Financial Services stated “This is yet another example of how we can innovate and work together with the private sector and the regulator to be at the forefront of new quality business for our Jurisdiction.The launch of SPV PCCs is the next step in our ambition to become the premier ILS jurisdiction within the European Union. The SPV PCCs will complement Gibraltar’s existing standalone insurance SPVs.”

PCCs corporate structure in which is a single legal entity comprising of a core and a number of segregated parts, or “cells” were introduced around the year 2000 as a means to commoditise Special Purpose Vehicles (SPVs) and as a basis of structuring investment products.

Guernsey, the first jurisdiction to introduce PCCs, experienced an increased collateralised reinsurance and ILS business growth thanks in part to the cells incorporations according to last year’s figures from the Guernsey Financial Services Commission (GFSC).

The establishment of a variety of models in recent time allowed Gibraltar’s extraordinary development of its insurance sector, and with the new PCCs offering could push Gibraltar to become a truly international insurance centre.

TalkTalk, one the leading telecom group, is downplaying the impacts on the cyber attack it suffered on Wednesday in which up to 4 million of its customers had their account details stolen.

In an update statement on Saturday, CEO Dido Harding said – ‘the investigation findings so far show that the number of customers affected and the amount of data potentially stolen is smaller than originally feared‘

She also added – ‘Any credit cards info which may have been stolen has the six middle numbers blanked out and can’t be used for financial transaction’

The company is working closely with the Metropolitan Police Cyber Crime Unit into the cyber attack. The investigations are still ongoing and no arrests have been made, yet.

On Friday, TalkTalk was contacted by someone claiming to be the hacker responsible for the cyber attack and demanding for a ransom. It is not yet clear whether the company is fully covered for this type of events or whether any cyber insurance policy has been triggered.

Nevertheless, TalkTalk is advising its 4 millions customers to change their passwords, even though those where not accessed during the breach, and is providing a free number (0800 083 2710) to report anything suspicious.

The company has also partnered with Noddle, one of the leading credit reference agencies, to offer 12 months of credit monitoring alerts for all its customers.

Chief Executive Officer Dido Harding latest update earlier today below

Another startup based in China is making a name for itself, Tongjubao, the peer-to-peer insurance innovator takes on community social risks (divorce, career disruption) by pooling the risks via its collaborative risk sharing platform.

So far, most of the innovations embarked on were challenging the broking sector within the industry as most them allow customers to form groups and then simply get cash back.

Lemonade is taking on a bigger undertaking because the company has applied to be a licensed carrier, which means that it can underwrite and offer policies itself.

Wininger, President and CTO, said “We’re challenging the way insurance companies work, with a peer-to-peer business model fueled by self-serve technology,”

“We are building an insurance company fully vertically integrated from the ground up to rethink some of the building blocks of the industry,” says Schreiber

The insurance industry is rigid with because all the different laws and regulations and this makes it a good target for disruption.

“It is very unusual for a company to receive $13 million in an initial round of funding,” said Haim Sadger, Partner at Sequoia Capital. “But it is rarer still to find such accomplished founders tackling such a sizable industry with such a compelling solution.”

We’re betting Lemonade will transform the insurance landscape beyond recognition.

It is one to watch.”

Another startup based in China is making a name for itself, Tongjubao, the peer-to-peer insurance innovator takes on community social risks (divorce, career disruption) by pooling the risks via its collaborative risk sharing platform.

So far, most of the innovations embarked on were challenging the broking sector within the industry as most them allow customers to form groups and then simply get cash back.

Lemonade is taking on a bigger undertaking because the company has applied to be a licensed carrier, which means that it can underwrite and offer policies itself.

Wininger, President and CTO, said “We’re challenging the way insurance companies work, with a peer-to-peer business model fueled by self-serve technology,”

“We are building an insurance company fully vertically integrated from the ground up to rethink some of the building blocks of the industry,” says Schreiber

The insurance industry is rigid with because all the different laws and regulations and this makes it a good target for disruption.

“It is very unusual for a company to receive $13 million in an initial round of funding,” said Haim Sadger, Partner at Sequoia Capital. “But it is rarer still to find such accomplished founders tackling such a sizable industry with such a compelling solution.”

We’re betting Lemonade will transform the insurance landscape beyond recognition.

It is one to watch.”