Dubai-based financial comparison platform Yallacompare has raised $8 million in its latest round of funding, led by venture capital firm Wamda Capital and STC Ventures.

New York’s Argo Ventures, the venture capital arm of international insurance provider Argo Group, also joined the financing round. Overall and with this latest investment, Yallacompare total capital reaches $17.4 million.

Originally, Yallacompare launched with the website domain named compareit4me.com in August 2011, which mainly focused on car insurance within the United Arab Emirates (UAE). However, the startup quickly expanded and underwent a rebranding to tap into region’s fast-growing general insurance market.

In addition to insurance, website customers can now compare many other financial products such as credit cards, different types of loans, bank accounts, and also purchase insurance through its online platform.

Yallacompare CEO Jon Richards believes that the “latest round of funding represents a ringing endorsement of our direct-to-consumer financial services model.”

Jonathan Rawling, Yallacompare’s chief financial officer, considers that the big challenge in the region is to bring offline customers to online. The awards winning startup could serve as a catalyst to support that ambition.

In fact, the trend is already changing as the number of people buying insurance online in the region increased by a multiple of four in 2018. Yallacompare doesn’t want to miss this opportunity so it will use the Series C funding to expand its workforce by 50% to boost its presence in Egypt, and also work on enhancing its market share in Kuwait and the United Arab Emirates.

The company already has a presence in Egypt, so it is likely that the funding will go toward hiring a dedicated team for that market.

MENA insurance opportunity

Yallacompare claims to control 76% of the online insurance sales market in the six countries of the Gulf Cooperation Council (GCC) last year. That’s a great position to be in as the size of the GCC insurance market is estimated to hit $44 billion in 2021. Thanks to double-digit growth in countries such as the UAE, Oman, and Saudi Arabia.

The growing proportion of online insurance sales means that Yallacompare’s revenue opportunity will increase in the GCC. But the company is clearly looking to expand into the broader Middle East and North Africa (MENA) region that encompasses 22 countries and presents a bigger opportunity.

Yallacompare is currently operating in three countries – Egypt, Jordan, and Lebanon – outside of the GCC that form a part of MENA. The company will probably look to increase its reach in this region going forward as the insurance industry will grow at a faster pace than the economy thanks to low penetration.

Insurance penetration in MENA countries is just a fourth of the global average. The growth of digital sales channels is expected to increase penetration in this area as it will allow online insurance players to pass on the benefit of lower operating costs to customers.

That’s why venture capitalists are betting on Yallacompare since it gives them a nice avenue to tap into this market.

According to Oleg Ilichev, head of Argo Ventures, “Our mission is to discover and empower entrepreneurs who are reinventing financial services. We believe that Yallacompare’s goal of educating and simplifying the purchase of financial products aligns nicely with our beliefs.

Ilichev praised the startup by adding: “Yallacompare’s management team has done an outstanding job of positioning the business as the leader in this space. We are excited to help the company expand across the region and offer new financial products to its customer base.”

Brazil’s newly elected President Jair Bolsonaro is proposing radical policies that could destabilize his nation and South America.

Observers fear instability because the far-right Bolsonaro is a controversial figure with bizarre political beliefs. For instance, Bolsonaro admires Brazil’s military dictatorship of the 1960s and 1970s, labels Climate Change a hoax, compares indigenous people to animals, and calls his opponents Communists, The Guardian reports.

Insurers must pay attention to the situation in Brazil because of the potential risks from Bolsonaro’s radical policies. Moreover, some of Bolsonaro’s policies could be a threat to Brazil’s neighbours.

Five Potential Risks posed by Bolsonaro include:

1. War between Brazil and Venezuela

Bolsonaro is an outspoken critic of Venezuela’s radical left-wing President Nicolás Maduro. In fact, in 2017, Bolsonaro pledged to “do whatever is possible to see that government deposed” in a statement about Maduro.

Brazil’s new president has announced no specific actions against Maduro. However, Brazilian newspapers have claimed Colombia’s government supports Brazilian military action to remove Maduro.

In addition, The Guardian reports some Venezuelans believe Brazilian military action against their country is imminent. Moreover, Maduro himself has said he thinks Bolsonaro is planning “a military adventure against the Venezuelan people.”

A major risk is a US-backed military operation or coup against Maduro. In fact, US President Donald Trump whom Bolsonaro admires, stated he is “not going to rule out a military option” for Venezuela. However, Trump did not say what a military option is.

Potential risks include combat between Brazilian and Venezuelan forces, or guerrilla war stemming from a Brazilian occupation of Venezuela. Another risk is that Maduro will launch pre-emptive military strikes against Brazil, or arm Brazilian leftists for guerrilla war against Bolsonaro.

2. Regional instability

Bolsonaro is open to the idea of a US military base in Brazil to counter “Russian influence” in South America, Fox Newsclaims. In particular, Bolsonaro fears Maduro’s close ties to Russia.

Such a base could prompt Maduro to host a Russian military base in Venezuela. A greater risk is Maduro will reach out to China for help.

Another risk is that other South American powers like Argentina will invite Chinese forces to their soil to counter “American imperialism”. China’s People’s Liberation Army is establishing bases overseas. Notably, China has major economic interests in Argentina it will want to protect, Reutersreports.

A final risk is a regional arms race with South American nations buying large amounts of weaponry they cannot afford to protect themselves from American, Brazilian, or Chinese imperialism.

3. Indigenous people unrest

Bolsonaro could trigger a conflict between Brazil’s government and indigenous people.

On his first day in office, 2 January 2019, the new president transferred certification of indigenous land from the National Indian Foundation to the agriculture ministry. In detail, that action could transfer ownership of indigenous land to miners and farmers, The New York Timesreports.

This could lead to conflict between miners and indigenous people over land. Notably, Bolsonaro’s agriculture minister Tereza Cristina Correa da Costa Dias is being accused of accepting money from a landowner accused of murdering an indigenous leader.

An obvious risk is fighting between indigenous people and Brazilian authorities. Another danger is that Maduro could arm indigenous Brazilians to tie down Bolsonaro’s military with guerrilla warfare. Thus, Bolsonaro could trigger unrest or guerrilla warfare in Brazil.

4. Sparking ethnic violence

Another risk is that Bolsonaro’s policies will spark civil unrest among the poor and African-Brazilians.

Residents look on as Brazilian military police officers patrol Mare, one of the largest complexes of favelas in Rio de Janeiro, Brazil, on March 30. – Mario Tama

Bolsonaro is dismantling a division of the education ministry designed to expand educational opportunities for black Brazilians, The New York Times reports. In addition, critics are announcing Bolsonaro’s action as unconstitutional.

5. Destabilizing Brazil

The situation in Brazil is reminiscent of that in Venezuela where elected radicals undermined democracy with extremist policies. The difference is that Venezuela’s radicals were extreme socialists, whereas Bolsonaro is of the far right.

Additionally, Bolsonaro’s personal story is like that of Hugo Chavez, the deceased founder of Venezuela’s authoritarian socialist regime. Like Chavez, Bolsonaro is a former paratrooper and populist with radical beliefs.

Chavez destabilized Venezuela by rewriting the constitution to make himself a dictator. Civil unrest, economic collapse, hyperinflation, and an attempted military coup marked Chavez’s years in power.

By 2017, Venezuela had become so chaotic its government cannot maintain law and order. For example, Medium writer Erik Brown charges that pirates are openly operating off Venezuela’s north coast. In particular, pirates killed 15 to 20 sailors in an attack on Guyana-based fishing vessels in Venezuelan waters in 2018.

Thus the greatest risk is that Bolsonaro’s chaotic leadership could completely destabilize Brazil and other parts of South America.

The European Union (EU) is worried about potential cyber security risks from Chinese technology companies. Several members are concerned with China’s behaviour in the cyber realm, and calling for regulations reinforcement in the upcoming 5G spectrum auctions.

Huawei, one of China most successful tech company, is often the cited culprit over the security concerns. The company is accused of being a tool that could be used by the Chinese government for espionage.

The fears come from China’s National Intelligence Law, which states that “organizations and citizens shall, in accordance with the law, support, cooperate with, and collaborate in national intelligence work.”

Western governments interpret this as a risk that Huawei would be forced to build “backdoors” in its equipment to give China access to sensitive data. Besides, the company has run into hot water recently, having its chief financial officer, Meng Wanzhou, arrested in Canada on 1 December 2018, for allegedly taking part in Iran sanctions fraud.

The United States, New Zealand, Australia and Japan have banned Huawei’s telecom infrastructure to varying degrees. In Europe, Brussels is encouraging its members to evaluate the options carefully before making decisions.

As once the auctions are complete, the involved members wouldn’t want to be in a scenario where an infrastructure provider with probable security risks is supplying equipment to an entire continent.

“We are urging everyone to avoid making any hasty moves they might regret later,”commented an unnamed diplomat who spoke to the Financial Times.

Several EU members have already hardened their stance on Huawei. The Czech Republic’s cybersecurity agency has issued a warning that Huawei’s products pose a cybersecurity threat, while the Belgian cybersecurity agency is reportedly considering a ban on the Chinese company’s products.

No evidence of backdoors

Meanwhile in the UK, British Telecom (BT) has decided to remove Huawei products from the core areas of its existing 3G and 4G equipment, and doesn’t plan to deploy its products during the 5G rollout either.

BT’s stance is surprising as Huawei has set aside £1.5 billion ($2 billion) to be spent over the next five years so that it can address the security concerns raised by the British intelligence and security agency GCHQ (Government Communications Headquarters).

Moreover, Huawei firmly denies any improper links with the Chinese government, and researchers including GCHQ have never found any evidence of such backdoors.

Germany’s Federal Office for Information Security recently found out that its network infrastructure wasn’t any less secure when compared to its rivals such as Europe’s Nokia and Ericsson, along with South Korean Samsung.

Despite the concerns, Huawei has already made headway in some EU member countries. T-Mobile Poland, for instance, launched the first fully functional 5G network in the centre of its capital Warsaw, and is tapping Huawei to build its 5G network further.

Altice PT, the largest telecommunications service provider in Portugal, signed a partnership deal with Huawei to develop and implement 5G services in Portugal. In all, the Chinese tech giant has made deals with telecom providers and had its infrastructure scrutinized in several other European countries.

That’s not surprising as Huawei has been known to provide telecom equipment at competitive rates, and there have been reports suggesting that the security concerns could be overblown.

The Chinese company is also allowing telecom operators to put security firewalls in its 5G network architecture so that they can view, monitor, and control the information flowing through. These efforts seem to be working in the company’s favour as the Huawei Cyber Security Evaluation Centre in the UK mentioned in its annual report that the company has “fulfilled its obligations” to the country’s government and telecom operators such as O2, EE, and Vodafone.

But the overall negativity surrounding Huawei means that the EU can be expected to play an important role in the region’s 5G infrastructure rollout by closely auditing and vetting the participants so that it can minimize any supplier-related risk.

Lloyd’s of London is unmoved by the recent release of hacked documents relating to the 9/11 terrorist attacks of 2001.

The insurer denies that its systems and corporate networks were compromised by any cyber incidents of late, especially from a hacker group calling itself ‘The Dark Overlord’.

Speaking to The Registeron Thursday, a Lloyd’s of London spokesperson said: “Lloyd’s has no evidence to suggest that the Corporation’s networks and systems have been compromised and remains vigilant with a number of protections in place to ensure the security and safety of data and information held by the Corporation.”

On New Year’s Eve, The Dark Overload hacker group posted online messages about possessing 18,000 secret documents of the 9/11 World Trade Center towers destruction and litigation/settlement cases. The group threatened to release the document files if no payment was made to their bitcoin account.

The Dark Overlord twitter thread

The hacker group says, it’s financially motivated and would release the files in layers and payment milestones. On Friday, the group made Layer 1, which includes several checkpoints, available after receiving a total of 3.27 BTC ($12,550) on their bitcoin address.

However, the files appear to be merely documents of emails communication between several law firms, such as Husch Blackwell (formerly Blackwell Sanders), and insurers like Hiscox that convey the litigations co-operation agreements and main parties background information.

Nonetheless, Hiscox immediately distanced itself from the rumours. In a statement, it said “The online posts relate to an incident we reported in April 2018 (view here), when we were made aware that a US law firm that advised Hiscox, some of our commercial policyholders and other insurers, had experienced a data breach in which information was stolen.”

The insurer added “The law firm’s systems are not connected to Hiscox’s IT infrastructure and Hiscox’s own systems were unaffected by this incident.”

On Wednesday, twitter suspended the hacker’s group account for breaching its policy by publishing hacked materials. The group then moved on Reddit but the account was also banned. In response, The Dark Overlord is now publishing its announcements on the blockchain powered social network Steemit.

Meanwhile, Lloyd’s said that they will continue to monitor the situation closely, including working with managing agents targeted by the hacker group.

America’s chief investment regulator, the Securities and Exchange Commission (SEC), is cracking down on robo advisers. In particular, the SEC is fining prominent robo advisers for misleading clients, improper advertising, and lack of compliance.

The SEC accuses Wealthfront of exaggerating the capabilities of its robo adviser, a press release states. For instance, Wealthfront allegedly claimed its robo adviser could monitor all of its client accounts to maintain a tax-loss harvesting strategy.

The SEC alleges the robo adviser did not monitor the accounts. Hence, the tax-loss harvesting strategy may not have been implemented as Wealthfront promised in advertising.

A tax-loss harvesting strategy can theoretically reduce clients’ tax liability by selling certain assets at specific times, as explained in their promotional video below. Thus, Wealthfront clients could have paid taxes they might have avoided.

In addition, Wealthfront tweeted unproven testimonials about its products and paid bloggers to promote its services, the SEC charges. Moreover, Wealthfront failed to maintain a compliance program required by US securities laws, the SEC charges.

Wealthfront will pay the SEC $250,000 (£197,631) to settle its case, Business Insider reports. In addition, Wealthfront will certify compliance and tell its clients about the order.

Robo adviser Hedgeable shuts down

The SEC alleges another robo adviser, Hedgeable, failed to comply with securities laws or properly document its transactions. Plus, Hedgeable is accused of making misleading statements about its robo adviser’s performance.

Hedgeable reportedly withdrew from the investment business in August 2017. However, Hedgeable’s app and website are still online. Additionally, the company paid an $80,000 penalty for offering misleading comparisons of its robo adviser’s performance to competitors.

In particular, Hedgeable offered performance comparisons that were not based on competitors’ actual-trading models, the SEC alleges. Moreover, Hedgeable’s robo-adviser platform did not include an effective regulatory compliance program, the SEC alleges.

Robinhood’s regulatory troubles

Another popular robo adviser platform Robinhood is accused of violating US banking regulations. Robinhood is a popular stock-picking robo adviser that suddenly dropped plans to offer “cash-management” accounts shortly before Christmas 2018.

Barron’s accuses Robinhood of offering savings and checking accounts not insured by the Federal Deposit Insurance Corporation (FDIC). To explain, the FDIC is a government agency that insures most bank accounts against loss in the USA.

Robinhood robo advisor app on Android store

However, Robinhood’s accounts were supposedly insured by a private trade association called the Securities Investor Protection Corporation (SIPC) not the FDIC, Barron’salleges. Notably, Robinhood stopped offering the accounts 36 hours after the allegations.

In fact, SPIC CEO Stephen Harbeck told Barron’s his organization was not insuring the Robinhood accounts. Tellingly, Barron’s reports Harbeck threatened to file an SEC complaint about Robinhood’s activities.

Senators want robo-advisers crackdown

Robinhood’s activities even attracted the attention of the United States Senate.

Seven US Senators wrote a memo asking the SEC and the FDIC to investigate Robinhood’s bank accounts on 20 December 2018, CNN reports. The senators asked the agencies to determine if Robinhood was misleading customers.

Plus, the senators want to know how the FDIC and SEC monitor fintech startups. Not coincidently, the SEC’s announced its actions against Hedgeable and Wealthfront on 21 December 2018.

Therefore, political pressure for a crackdown on robo advisers and similar products like cryptocurrency exchanges is growing in the United States. Under those circumstances, more companies are likely to follow Hedgeable’s lead and pull out of the robo-adviser business.

Risks from robo advisers

The SEC actions and the Robinhood saga indicate there could be significant risks from robo advisers and other next-generation investments platforms.

Significantly, the Robinhood story indicates many of the platforms offered by such platforms are not insured. Thus, there is a risk the robo advisers could run out of money and require a government bailout.

Managed assets like hedge funds run by robo advisers can cause financial crises or make them worse. For instance, the infamous hedge fund Long-Term Capital Management (LTCM) nearly triggered a global financial crisis when it ran out of money in 1998.

Only a bailout organized by the US Federal Reserve prevented LTCM’s complete collapse. The fear is that funds controlled by robo advisers or artificial intelligence (AI) could collapse as LTCM did.

Thus risk managers need to examine the dangers created by new technologies like cryptocurrencies, decentralized exchanges, AI, and robo advisers. Moreover, there is a need for new insurance products to cover the risks created by robo advisers.

Hong Kong-based digital insurance start-up Bowtie has raised $30 million in its Series A funding round, led by Canadian insurance company Sun Life Financial.

This marks a significant milestone for Bowtie, which recently became Hong Kong’s first online only insurer to receive a virtual license from the region’s insurance regulator, the Insurance Authority (IA).

Hong Kong’s IA is serious about pushing the digital transformation in the insurance industry, so it chose to launch a fast-track approval system to provide virtual insurer licenses in September 2017. The program has garnered a lot of interest, as more than 40 companies have applied for these licenses, serving the IA’s vision of “pushing insurtech in Hong Kong to give more choice for customers.” Bowtie is the first beneficiary of this vision.

Bowtie’s vision

Bowtie, which was founded in 2017, will use this funding to launch its online-only, health and life insurance products to customers in Hong Kong in the first half of 2019.

Fred Ngan (left) receiving Best FinTech Awards 2017

That should allow the digital insurance start-up to disrupt the multibillion-dollar insurance market in Hong Kong thanks to its low-cost nature of operations.

Bowtie’s virtual insurer license means that it won’t be able to maintain any physical locations. It can only offer its services direct to the customer through digital channels such as computers or smartphones, eliminating the need for banks, agents, physical paperwork, and location-related costs.

As a result, Bowtie can pass the benefits of its online-only model by offering commission-free health insurance to clients.

Fred Ngan, the Co-founder and Co-CEO of Bowtie, said: “The online business model allows us to run at low cost – we only need about 50 people to develop the technology and provide customers services. We don’t need to share any commission with agents or banks so we have a cheaper distribution channel than the traditional insurance companies.”

Ngan is going after the low-hanging fruit in the Hong Kong insurance space. He goes on to point out that Bowtie doesn’t intend to compete with traditional insurance companies who sell complex policies with high sums.

Instead, Bowtie is looking at simple products in the life and medical insurance niches that don’t attract the attention of traditional insurers and agents because of low margins.

However, Bowtie can maintain a low cost base thanks to its online-centric model, which allows it to go into areas where legacy insurers wouldn’t pay much attention. This vision seems to have attracted some big names.

Apart from insurance behemoth Sun Life, Bowtie’s Series A backers also includes Hong Kong X Technology Fund, which is backed by Sequoia Capital managing partner Neil Shen and Tencent founder Pony Ma.

Sun Life InsurTech strategy

Sun Life believes that this investment will allow it to go after an under-served opportunity in the Hong Kong insurance space. Fabien Judy, Sun Life Hong Kong CEO, opines that people are under-insured in the life and health insurance sectors in the region.

He points out that the Bowtie investment is a part of Sun Life’s digital transformation, which would possibly help it attract more customers through the online channel. However, the two companies will operate as separate entities.

Sun Life’s investment in Bowtie makes sense as the online insurance is gaining tremendous traction. An EY survey has found out that over 80% insurance customers across the world are open to using digital interfaces such as smartphone applications instead of going through traditional channels that involve brokers, agents, or banks.

GoCompare, one of the UK’s top price comparison aggregators, has partnered up with fraud prevention expert Featurespace to improve the detection and prevention of fraudulent activities on its website.

Online fraud has become a major issue for many industries, and is now the most commonly experienced crime in England and Wales. According the ONS (Office National Statistics), it accounts for 42% of all estimated offences, approximately one in six offences are incidents of online fraud.

Over the years, GoCompare has built one of the most popular online insurance comparison and switching platform in the UK. Its success has also brought problems such as fraud, which it had to address with mixed results.

Fraudsters, being smart people, use clever but unscrupulous tricks to manipulate online comparison platforms (aggregators). They tend to use quote manipulation, application fraud, ghost broking, and many other practices. All of these have had negative effects on the platforms, especially in terms of trust.

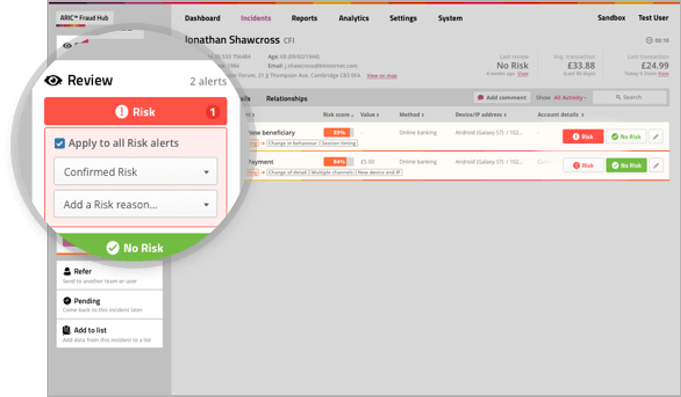

Featurespace, Cambridge-based adaptive behavioural analytics world leader, developed a machine learning software hub that can monitor customers’ data in real time. The hub branded as ARIC (Adaptive, Real-time, Individual, Change-identification) Fraud Hub features functionalities that spot anomalies, block new fraud, and recognise genuine customers.

GoCompare, with the help of Featurespace’s ARIC Fraud Hub, intends to tackle fraudulent transactions activities furthermore, thus adding to its existing efforts in combating fraud.

Fleur Lewis, GoCompare’s Head of Fraud said: “We recognise that comparison websites act as the gatekeepers of data for many insurers and that we have an important role to play in the prevention of front-end fraud.”

“We recognise that comparison websites act as the gatekeepers of data for many insurers and that we have an important role to play in the prevention of front-end fraud.”

Fleur Lewis, GoCompare’s Head of Fraud

Lewis sentiment is shared by the Insurance Fraud Taskforce recent 2017 report, which also recommends the aggregators to interact with existing fraud databases, such as the Claims and Underwriting Exchange (CUE), and data sharing schemes on a consistent basis. This could help improve the industry’s ability to detect fraud at the point of quote.

Monitoring customers’ behaviours

Claims history, points on a driving licence, and or car modifications are some of the material facts would-be customers deliberately fail to disclose in order to lower their insurance premium.

One of key features of Featurespace’s ARIC Fraud Hub is that the system monitors the real-time behaviour of each applicant, and therefore can detect and alert any anomalies spotted.

According to their website, Featurespace’s ARIC Fraud Hub platform uses Bayesian statistics algorithms to build the individual customers profiles. Bayesian statistics refer to the branch of statistics that relies on the Bayesian inference model. The model is one of the key building blocks of machine learning (ML) and artificial intelligence (AI) technologies in recent times.

Featurespace’s ARIC Fraud Hub platform

The model works by applying probability to statistical problems. This simply means that the probability of observing an event A, given a prior realised event B plus background information, is inferred. Essentially, the approach attempts to link established background information with incoming evidence to predict the probability

In practice, GoCompare will now be able to compile a model of every potential customer’s likely behaviours based on their online transactions. If a customer interacts with the website in a way that doesn’t match their profile, the Featurespace software will alert the GoCompare’s fraud prevention team

One fraud every minute

These new capabilities will not only help GoCompare ensure a frictionless customer experience but also provide its insurance partners with genuine customers – thereby reducing their operational costs and losses.

Last August, the ABI (Association of British Insurers) revealed the true extent of insurance fraud in the UK, where one insurance fraud is detected every minute. In total, detected and undetected fraud costs an estimated £3 billion each year.

The effects of fraud are premium increases for genuine customers, GoCompare with the new Featurespace partnership aims to reduce that burden.

Deutsche Bank settled a €4 million fraud investigation with German public prosecutors for its role in helping clients carry out dubious tax deals, Bloombergreports.

The settlement puts an end to a probe known as ‘Cum-Ex’ deals. The Frankfurt-based prosecutors identified the troubled bank as one of the parties facilitating the controversial tax schemes.

While Deutsche Bank denies its involvement as being the intermediary of the tax deals, it recognizes its role in the activities of some of its clients. The charge against the bank relates to deals done by individuals investigated in the probe, which the bank acted as a custodian for.

Bloomberg reveals that a payment of €540,000 (£486,000) was made to the prosecutor’s office. This resulted in the cases against three of the six individual suspects being dropped. The agency currently handles eight cum-ex probes. The €4 million fine ends parts of the cum-ex investigation which relates to raids made in September 2015.

Cum-Ex trading

The so-called ‘Cum-Ex’ deals were based on complex tax schemes that allowed owners of shares to claim refunds, more than once, for tax paid on dividends payouts – thus effectively syphoning off taxpayers’ money into investors’ pockets.

Profitable companies, that decided to reward investors who owned their shares, did so by paying a sum of money out of their profits (or reserves) at the end of their financial year. This payment is called the dividends.

Upon receiving their payments, investors are charged a dividend tax at source. In Germany, it’s currently at 25%. However, foreign investors can request a refund from the tax authorities.

Around the dividends payment day, shares of large companies were sold and bought back via a network of banks, stock traders and lawyers. The shares changed hands so quickly that the tax authorities were unable to identify who the true owners were.

Working together, investors then claimed multiple refunds for tax paid on the dividends and pocketing the profits amongst themselves, while the treasury footed the bill.

The man behind this scheme is allegedly former government tax expert, Hanno Berger, who jumped ship to become one of Germany’s most profitable tax attorneys. His clients included Adidas, Karstadt and the family that owns BMW.

It took a cross-border investigation of 38 reporters, 19 media over 12 countries, digging 180,000 pages of documents to expose possibly one the biggest tax robbery in European history.

The European Parliament acknowledges the estimates that the fraud have cost Germany around €25 billion, France €17 billion, Italy €4.5 billion, Denmark €1.7 billion and Belgium €201 million.

Stronger EU tax authorities needed

During a plenary session held on the 29 November, European Union MEPs called for an inquiry, rule changes and stronger tax authorities to avoid a repeat of the cum-ex tax fraud scandal, which cost member states more than €55 billion.

ESMA & EBA inquiry

MEPs have called on the EU’s European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) to conduct an inquiry into the schemes that defrauded member’s tax authorities.

The financial regulatory agencies need to assess the potential threats to the overall EU financial markets and establish the participants involved. In addition, they need to evaluate if national or EU laws were breached. The agencies should also examine whether national supervisors took actions against the wrongdoers.

EU rule changes

In spite of recently adopting the sixth update of the Directive on Administration Cooperation – DAC6, MEPs urge for additional changes to the Directive that also oblige the disclosure of schemes established for dividend arbitrage.

The adopted DAC6 aims to enhance tax transparency and combat aggressive tax planning across the European Union (EU)

Improve tax surveillance

MEPs also call on the Commission to propose a European framework for cross-border tax investigations, the setting up of an EU Financial Intelligence Unit, and an early warning mechanism.

Member states must invest in and modernise their tools, provide adequate human resources to improve surveillance, and ensure better information sharing between tax authorities

Only then EU tax administrators can successfully deal with any new aggressive cross-border tax schemes.

For the time being, Deutsche Bank is let off the hook with this settlement. However the company is still battling further pending investigations.

General Electric (GE), one of the most iconic names in American business, is cracking up because of debts. A company founded by Thomas Edison is selling assets to survive.

“This is a slow-motion break-up of the company,” Stifel analyst Robert McCarthy tells CNN Money. For example, GE is selling off core businesses such as lighting and healthcare to raise cash.

In addition, some of GE’s oldest and most prestigious components including its railroad division are probably for sale. The plan is to raise enough cash to pay off debts and pension obligations.

General Electric had $114.9 billion debt and $263.5 billion in liabilities on 30 September 2018. Yet it generated $122.1 billion in revenues in 2017, Stockrow reports. Thus, GE cannot pay its debts with current resources.

Not surprisingly, General Electric reported a net loss of $22.8 billion and an operating loss of $20.9 billion on 30 September 2018. Under those circumstances, the only way GE can raise money is to sell assets.

However, the value of those assets may not cover General Electric’s debts. For instance, analysts value the lighting business at $600 million to $800 million, LED Insidereports.

GE could face bankruptcy

Yet General Electric faces over $15 billion in obligations from its failed finance company GE Capital, The Financial Times estimates. Thus GE could be incapable of paying its debts and facing bankruptcy.

Additionally, General Electric’s pension fund is facing a $29 billion shortfall, Forbes contributor Ken Kam calculates. To explain, the amount of pension payments GE is obligated to make exceeds the cash in the pension fund by $29 billion.

Markedly, Kam thinks bankruptcy is the only way GE can avoid making those pension payments. To clarify, if General Electric declares bankruptcy it can transfer the pension obligations to a government agency called the Pension Benefit Guarantee Corporation (PBGC).

USA corporate debts risks

The situation at General Electric puts a spotlight on USA’s corporate debts and pension crises. In detail, GE is one of many America corporate giants with massive amounts of debt and pension obligations.

For instance, struggling automaker General Motors (GM) recorded total debts of $102.3 billion on 29 November 2018. Consequently, General Motors announced a massive cost-cutting plan on 20 November 2018. The cost-cutting plan will eliminate 14,000 jobs, several factories, and several vehicles, The Detroit Free Pressreports.

GE and GM are trying to avoid the fate of retail legend Sears which declared bankruptcy on 15 October 2018. Sears filed bankruptcy because it could not meet a $134 million debt payment.

Like GE, Sears is selling assets including its iconic Craftsman tools and Kenmore appliances brands. Sears is trying to avoid liquidation with a total reorganization and loans from Cyrus Capital Partners.

Moreover, Sears is struggling with pensions just like GE. Former Sears CEO Eddie Lampert admits contributing $4.5 billion to pension plans between 2005 and 2018. Sears must make payments to 90,000 pensioners.

General Motors, for its part, contributed $1.1 billion to US pension plans in 2017, according to Pensions & Benefits. In addition, GM contributed $1.2 billion to Canadian and UK pension plans in 2017.

It is estimated that the total US corporate pension plan obligations were $68.5 billion on 31 December 2017. However, America’s corporate pension plans had $62.9 billion in assets on the same day. Thus America is facing a corporate pension crisis.

General Electric at a glance

Finance legends JP Morgan and Anthony Drexel formed the company that became General Electric in 1889 by merging two companies. One of GE’s predecessors was the firm Edison organized to commercialize his light bulb.

Today, General Electric’s products include commercial and consumer finance, locomotives, jet engines, water treatment systems, power grids, appliances, and generating plants. General Electric’s former subsidiaries include the American television network NBC, which it sold in 2011.

General Electric was one of the companies that built America. GE’s debt-driven crack up could be the beginning of a new American economic crisis.

After 20 months of negotiations, the 27 European Union (EU) leaders finally agreed to the UK’s Brexit deal at last Sunday 25 November 2018 Brussels summit.

A satisfied Theresa May, UK Prime Minister, urged both Leave and Remain voters to unite behind the agreement, as it marks the culmination of UK exit negotiations with the EU and also the start of a crucial national debate.

During her briefing, May said: “The British people don’t want us spend any more time arguing about Brexit. They want a good deal done that fulfils the vote and allows us to come together again as a country … In parliament and beyond it, I’ll make the case of this deal with all my heart and I look forward to that campaign.”

On 11 December, May will put her Brexit deal to Members of Parliament (MPs) in the House of Commons, with the intention of getting an approval. So as to facilitate the UK’s exit from the European Union planned on the 29 March 2019.

However, the narrow nature of the Leave victory in the 2016 referendum has made Brexit a deeply divisive issue in the country ever since. While some favour the deal, many on both sides of the argument have come out against it.

Deal strong oppositions

For many Leave voters, the agreement shackles the UK to a Customs Union and Single Market for an indefinite amount of time. This part of the deal – known as the backstop – was designed to stop Northern Ireland being treated differently from the rest of the UK, in assuming regulatory alignment with the Republic of Ireland, and therefore the rest of the EU.

Prime Minister May has instead agreed that the entire UK remain in the Customs Union and Single Market temporarily, until such time as a permanent solution to the thorny issue of the UK’s border with the Republic of Ireland can be resolved.

Critics argue that the timeframe for this is too vague and could effectively leave the UK in a situation where they are part of the Customs Union and Single Market, but have little or no influence over it. Britain will no longer be a EU member state but would still have to pay billions of pounds every year for access to it.

While May has claimed that the deal has ended freedom of movement for EU citizens in the UK, and conversely for UK citizens across the European Union. It has also guaranteed the rights of those EU citizens already living in the UK, and will do so for any of those arriving in the country after the 29 March 2019 deadline.

The Labour opposition in Parliament have come out against the deal because it does not meet the party’s six tests. Labour leader Jeremy Corbyn says it fails to guarantee the rights of British workers which they currently enjoy as being part of the European Union. But more importantly, he added that it’s a bad deal for the country and Labour will oppose it.

Theresa May is trying to sell yesterday’s summit as a great success but to borrow a phrase “nothing has changed”.

With her own Conservative Party deeply divided on the deal, and opposition parties such as Labour and the Scottish National Party all vowing to vote against it, there is still a possibility that it will be passed nonetheless.

Brexit Deal voted down

So what are the alternatives? While the Prime Minister insists she is not looking beyond the 11 December vote, it would be wise to consider the ‘what ifs’ and the risk of a no deal.

Firstly, if the deal is voted down, then Corbyn has said he believes that will be a rejection of the Prime Minister herself and attempt to force a no-confidence vote in Theresa May which he hopes would then trigger a General Election.

Both party leaders do seem to be in agreement that the UK cannot leave the EU without a deal. There are a number of different scenarios which may play out if the Prime Minister’s deal is voted down.

If Theresa May is ousted or indeed resigns as party leader, she will be replaced with another Conservative leader who may believe they can negotiate a more favourable deal with the EU. Although that looks unlikely given that the EU leaders have already insisted that the deal on the table is the only one they will be considered.

Likewise, if Corbyn gets a General Election and becomes Prime Minister, he might seek to strike a new deal with the European Union, although he may run into the same difficulties as a Conservative Party leader.

The other option is, whoever is Prime Minister following the Parliamentary vote, takes the question back to the public and holds a second referendum. May has insisted she will not do that, and Corbyn seems reluctant too, although he has not come out strongly against it. Hence, there may have to be a change of leadership in either party for that to happen.

No Deal scenario

When no deal is talked about, it is often in the context of the UK ‘crashing out’ of the EU without a deal. That gives an indication of the potentially damaging affect a no deal would have.

While it is difficult to see Parliament allowing this to happen if the current deal is rejected, it would remain a possibility in the absence of anything else.

According to HM Treasury, a no-deal Brexit would have significantly damaging effect on many aspects of British life.

Goods which the UK exports to Europe would be immediately slapped with tariffs and subjected to inspections. It is estimated that farm exports could be hardest hit, with potential tariffs of up to 40%.

Checks at ports and airports could also lead to massive delays and disruptions, both for lorry drivers and travellers. A slowing down of the transport of goods and costly tariffs would severely disrupt the supply chain of many foods and there could be shortage of some foods while supermarket prices would rise sharply.

Under a no deal, British citizens living in EU countries would instantly have no legal status and this would apply to EU citizens in the UK.

The doomsday alternative of a no deal is perhaps what Prime Minister May is hoping will sway MPs to get behind her deal, but it is risky strategy and all eyes will be one the House of Commons on 11 December to see if it pays off.