Slightly more than one in five US college students, 21.2%, admitted to financing cryptocurrency purchases with student-loan funds, a study by The Student Loan Report found.

The funds were supposed to cover students living expenses at college. Instead, they were being used to buy virtual currencies, such as Ethereum (ETH) and Bitcoin (BTC).

The study carried out a survey of 1,000 current college students with loan debt with a single question: “Have you ever used student loan money to invest in cryptocurrencies like Bitcoin?”

The survey did not ask how much students were investing, and many could be simply testing the waters by buying only smaller amounts.

Depending on their financial needs, undergraduate students can receive up to $5,500 in federal loans in the 2017-2018 academic year, according to Federal Student Aid, a part of the US Department of Education.

Last year, cryptocurrency growth was phenomenal and clearly this could be one the reasons for students to venture into the digital asset.

However, cryptocurrency speculation is dangerous because it exposes both borrowers and lenders to an extremely volatile market. The most popular cryptocurrency; Bitcoin rose to an all-time high price of around $19,205.11 (£13,502.92) on 17 December 2017 then dropped to a low of $6,701.40 (£4,711.69) a little over four months later on 5 April 2018, Coinbase data indicates.

The second most popular cryptocurrency, Ethereum, lost more than two-thirds of its value during the first quarter of 2018. Ethereum was trading at $1,338.67 (£941.21) on 13 January 2018 and $503.01 (£353.66) on 17 April 2018. Coinbase estimated that Ethereum’s price increased by 940.14% in the 12 months that ended on 17 April 2018.

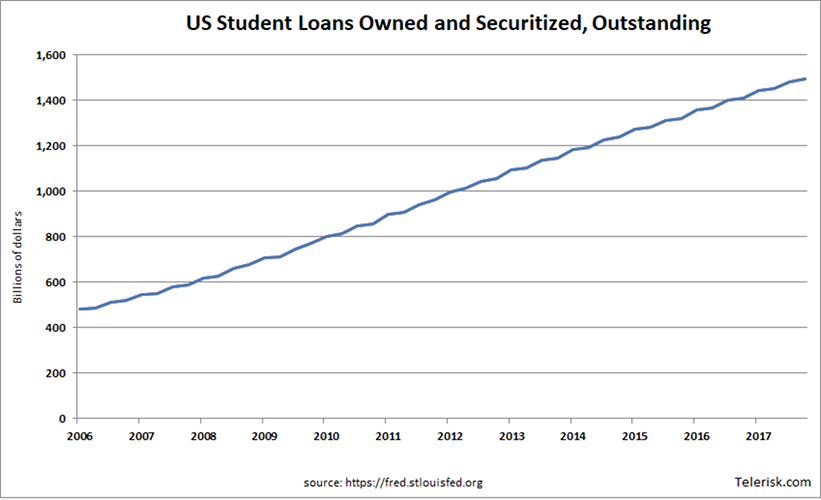

The risk to lenders is tremendous because around 44 million Americans owed around $1.48 trillion (£1.04 trillion) in January 2018, Student Loan Hero reported. The average American college student owed $37,127 (£26,103.62) in student loans upon graduation. That amount increased by 6% between 2016 and 2017. The amount of student loan debt owed in the United States exceeds credit card debts which were estimated at $1.03 trillion (£720 billion) in January 2018.

No oversights of student loans

The students are able to speculate in cryptocurrencies because there is no oversight on how the loan money is used, StudentLoans.net revealed.

In the United States, lenders send colleges a lump sum of money to cover tuition. If the funds paid out exceed the amount of tuition, the leftover cash is given directly to the students.

The students can use the funds for whatever they want including holiday trips, beer, gambling, speculation, video games, or new cars.

Disturbingly, buying cryptocurrency might be the most responsible use students are making of that money. There is at least a possibility the students might make a profit from the digital currency. Funds spent for beer or holiday trips will be completely lost.

Risks to the greater economy

The student loan situation will remind many observers of the US subprime mortgage crisis of the mid-2000s.

That crisis developed because of irresponsible lending to low-income individuals many of whom used the mortgage money borrowed for other purposes. Some borrowers used second mortgages to cover living expenses or finance holidays, and calls. Many people used the subprime mortgages to speculate in real estate – the infamous flipping.

The subprime crisis was one of the underlying causes of the financial crisis of 2007 to 2008. That crisis developed because investment banks, hedge funds, and other financial institutions were heavily-invested in mortgage-backed securities.

The student loan market is already in crisis, around 11.5% of student loans were in default in October 2017, US Department of Education data indicates. The number of student loans in default was estimated 8.5 million and the number of loans in default increased by 12% between June 2016 and June 2017, Forbes reported.

Technology fuelling speculation

The exposure of the economy and individuals to volatile speculative markets is greater than ever because of new financial technologies such as cryptocurrencies. The student loan situation reveals that individuals at all levels of the economy are exposed to the cryptocurrency risks.

The amount invested in cryptocurrencies is now large enough to create risks for the wider economy. The total market capitalization of all cryptocurrencies reached $741.620 billion (£521.43 billion) on 8 January 2018, CoinMarketCap calculated. That figure fell to $257.704 billion (£181.19 billion) by 4 April 2018. That means cryptocurrency lost nearly $500 billion (£351.55 billion) in value in four months.

Exposure to new speculative investments like cryptocurrencies is a risk that all insurers and lenders will have to take into account. New technologies are greatly increasing volatility and spreading the exposure to that volatility far and wide.