US Commodity Futures Trading Commission (CFTC) followed regulators around the world in issuing a stern warning regarding the potential pitfalls of cryptocurrency speculation.

The regulator urges investors to be wary of participating in the latest digital cryptocurrency schemes, and that they should not purchase virtual currencies, digital coins, or tokens based on social media tips or sudden price spikes.

In doing so, the CFTC follows other international actors in issuing warnings to speculative investors. The United Arab Emirates’ financial regulator, the Securities and Commodities Authority, urged caution regarding ICOs not long ago, and the International Organization of Securities Commission released a notice alerting investors to the risks associated with ICOs.

China’s central bank was the first in the world to entirely ban ICOs, a seemingly radical solution to solve the shortcomings of token sales. Even South Korea – a market which was initially quick to embrace cryptocurrencies – followed suit in implementing an ICO ban, leaving many to wonder how the regulatory frameworks in western countries might be shaped.

These bans are the result of practically uncontrollable structural security failings in the crypto community. As hackers and scammers are attracted to the amount and velocity of transaction in the crypto sphere, a large percentage of funds raised in ICOs never reach the ICO arrangers. In banning ICOs altogether, China and South Korea seek to eliminate this uncertainty.

ICOs security inadequate

In a recent publication by EY (formerly Ernst & Young), these dangers of poor security infrastructure were highlighted, as it can lead to a loss of funds and personal data. When personal data is hacked, it often ends up making its way to the black market, where it can be used for identity theft or fraud.

The US Commodity Futures Trading Commission recently joined other regulatory bodies in highlighting the possibility of “pump-and-dump” schemes in the cryptocurrency market. However, this came just a day after CFTC Commissioner Brian Quintenz and CFTC Chairman Christopher Giancarlo publicly implored crypto-companies to take the matter of regulation into their own hands.

In a testimony to the Senate Agricultural Committee, Giancarlo stated that crypto companies should scramble to sanitize the crypto sector. ”They need to know they’ve got a responsibility in cleaning up this industry if they really wanted to be something that bears the respect and becomes part of not only our future but their future as well”, he said in from of the Senate committee.

ICOs are not only under fire from governments and NGOs; they are also facing adversity from social media behemoth Facebook. Last month, Facebook decided that it would no longer be showing ads for cryptocurrencies or ICOs. In a statement, Facebook Product Management Director Rob Leathern explained that the move is the result of an “intentionally broad” policy against fraudulent marketing.

Whilst Google has not yet implemented any comparable bans on cryptocurrency ads, many are calling for them to take a similar stance. It would certainly not be unprecedented – Google has previously banned high-rate payday loan advertisements. However as of yet, not formal decision regarding cryptocurrency ads has been announced.

This range of different attitudes regarding how cryptocurrencies should be regulated has created a lot of uncertainty moving forward. Without any clear international strategy for whether cryptocurrencies should be encouraged, discouraged or even banned, stakeholders are in a state of limbo as they await a comprehensive regulatory framework.

In contrast, other countries are embracing the shift towards virtual currencies. The municipality of Zug in Switzerland is a gleaming example of this. Known as the Crypto Valley, Zug has become a crypto hotbed during the last years.

Unlike the bans in China and South Korea, Switzerland has pushed for more lenient cryptocurrency regulations, spearheading domestic regulation for four different types of ICOs. This comes as Swiss economics minister Johann Schneider-Ammann recently stated that he wanted Switzerland “to be the crypto nation”.

Notwithstanding the uncertainty regarding how crypto regulation should look, there is an even bigger hurdle that the blockchain process needs to clear before reaching mainstream adoption. This is that of security.

The size of the cryptocurrency sphere has attracted the attention of hackers and scammers alike. The absence of a centralized authority, information chaos, and the blockchain’s irreversibility hold notable allure for hackers, and as a result, on average more than ten percent of ICO funds are lost.

A recent phishing scam that is symptomatic of the hit the decentralized home-sharing network Bee Token. Hackers posing as ICO operators managed to swindle potential investors of nearly $1 million dollars, in just 25 hours.

This is partly as a result of that blockchain project founders often focus on attracting investors leading up to the ICO, rather than prioritizing in building a secure platform infrastructure. The most common form of ICO theft is through phishing, since a phishing website clone can be virtually impossible to distinguish from the original.

Cryptocurrency startup LoopX recently performed an “exit scam”. After raising $4.5 million in a series of ICOs, the company went dark – deleting all of their social media accounts, and taking their website offline.

A similar story is that of Prodeum. This company promised to “revolutionize the fruit and vegetable industry”, before wiping their entire website – leaving only written profanity behind on a white background.

ICOs regulation exigency

This makes it clear that the blockchain has some major bumps in the road to pass, before reading the mainstream adoption highway. However, any solution would have to be a multifaceted one. Whilst blockchain technology seems to urgently need more regulation, many fear that overly tight regulations might end up stifling the budding industry as a whole.

As cryptocurrencies might very well symbolize the next step in digital payments, this is something that policymakers want to avoid. Even if global regulations were implemented in a satisfactory and consistent manner, there is still the question of security.

With large amounts of money ”leaking” from ICOs due to chronic issues with hacking, this might dissuade large actors from conducting ICOs. For example, Telegram is reportedly about to launch an ICO with so-called GRAM tokens.

Such a crowdsale could, according to some, raise as much as $2.55 billion. The risk that around 10% of this could go missing due to hacking is simply unacceptable for Telegram.

Phishing attacks are hard to defend against, and calling on developers to improve the security in their new-born ICO blockchain platforms is simply too costly to be an effective solution.

The blockchain represents a fascinating segment of new technologies – albeit one that needs scrutiny both regarding regulation and security.

Every insurer needs to ascertain the potential risks of the sudden termination or modification of international trade agreements. The havoc wreaked by the Brexit vote in the UK demonstrates the vast damage and great confusion that sudden changes in trade policy can cause.

A paradigm shift in trade policy that has the potential to be as dramatic and as disruptive as Brexit is possible on the other side of the Atlantic. There is growing speculation that US President Donald Trump might try to pull out of the North American Free Trade Agreement (NAFTA).

NAFTA is a free trade zone consisting of the United States, Canada, and Mexico. Ending it would disrupt international trade because Canada and Mexico are the second and third largest trading partners of the United States. Canada accounted for 16.4% of US foreign trade worth $636 billion (£458 billion), and Mexico accounted for 15% of America’s trade with an estimated value of $582.4 billion (£419 billion) in 2017, the US Census Bureau estimated.

NAFTA’s end would harm Mexico

Even speculation about the end of NAFTA can affect the international economy.

News that Canadian officials believed Trump would try to end NAFTA caused the value of US stock indexes to fall and the prices of Canadian and Mexican currencies to drop in the markets on 10 January 2018, Reutersreported. The S&P/BM IPC stock index in Mexico fell by around 1.8% because of NAFTA speculation.

The possible effects of NAFTA’s end are widely debated. Damage in Mexico might be vast because that country is heavily dependent on US trade. The economic crisis of 2008 caused the Mexican economy to contract by 9% in 2009, Luis Rubio of the Wilson Centre’s Mexican Institute noted. Mexico’s domestic economy nearly collapsed because of the fall in US trade.

“That event demonstrated that the NAFTA is the only engine of growth of the Mexican economy,” Rubio wrote. “Modifying the economic framework that is inherent to NAFTA would imply putting the engine of the Mexican economy at risk.”

NAFTA’s end a ‘Manageable Risk’ for Canada

The effects of NAFTA’s end in Canada would be a bad but “manageable risk,” a Bank of Montreal (BMO) study named The Day after NAFTA observed. The BMO concluded that ending NAFTA would cause Canada’s economy to contract by 0.7% to 1%, The CBC reported.

The major damage would be done by a weaker exchange rate which can lead to a cheaper Canadian dollar and inflation. That would benefit Canadian industry by lowering the price of its’ products on the world market – but hurt average Canadians by raising prices for imported consumer goods.

Canada would lose $15 billion (£10.79 billion) worth of buying power and between 25,000 and 55,000 jobs if NAFTA ended, Don Ciuriak of the C.D. Howe Institute told the CBC. Ciuriak also predicted that the US economy would be hurt.

“The United States suffers about as large a drop in its bilateral exports to NAFTA partners as it reduces imports from them,” Ciuriak is predicting.

Can Trump really end NAFTA?

The greatest risks presented by sudden changes in trade policy were demonstrated by the fallout from Brexit in the UK. Those risks are the fear, uncertainty, and doubt (FUD) generated by such an unprecedented event.

Uncertainty from NAFTA’s potential end would be greater because it is not unclear if Trump would be able to make good on such a threat. Current law gives Trump the power to end or renegotiate NAFTA by giving six months’ notice.

America’s Constitution gives the US Senate to simply override Trump’s decision at any time. The Senate has the power to undo any Trump decision on NAFTA with a vote of 60 of its 100 members. Any vote of less than 60 US Senators can be blocked by an arcane legislative stratagem known as a filibuster.

NAFTA’s fate in US Senate hands

What is unknown is whether 60 US Senators can be convinced to overturn NAFTA’s end.

Most members of the Senate are conservative Republicans and moderate Democrats that strongly favour free trade. There are a few outspoken critics of NAFTA in that body, including leftists Bernie Sanders and Jeff Merkley.

Something to keep in mind is that Border States like Texas and California, which benefit from NAFTA, each have two Senators. At least two influential border-state senators; John McCain and Jeff Flake are open political enemies of Trump.

A decisive factor in Senators’ votes will be Americans of Mexican descent. There are around 36 million Mexican Americans, who make up more than 10% of the nation’s population (327 million), Pew Research calculated. Senators from states with large Mexican populations are likely to vote for NAFTA and against Trump.

The probable risk from an effort to end NAFTA is a high level of FUD that will be made greater by a vicious and protracted political battle in the Senate. It is not known if Trump is willing to risk such a battle which would split his party, the Republicans, along ideological and regional lines.

Is Trump bluffing about NAFTA?

An outside event that might delay a NAFTA action is the US Congressional election scheduled for November 6, 2018. Some observers have predicted that the Republicans might lose their majority in at least one house of Congress in that contest.

Therefore it is unclear if speculation of NAFTA’s end is real or a bluff by Trump. Trump’s pushing of a decisive issue like NAFTA during such an election seems improbable.

The greatest risks created by speculation about NAFTA’s end or renegotiation are the FUD that talk of such an event generates. The high levels of FUD are likely to have negative effects on all three North American economies for the foreseeable future.

The US government is abandoning efforts to impose stricter regulation on insurance companies’ financial activities. The new policy is coming at a time when serious questions are being raised about the financial health of some American insurers.

The US Treasury Department is dropping an appeal in a court case involving MetLife and the Financial Stability Oversight Council’s (FSOC), Pensions & Investmentsreported. The case; MetLife, Inc. v. Financial Stability Oversight Council, involved the FSOC’s designation of the insurer as a “nonbank financial institution.” Such a designation would have subjected MetLife to more oversight and regulation.

“I am pleased that the Justice Department has settled the MetLife case, consistent with the recommendation by a majority of FSOC voting members,” Secretary of the Treasury Steven T. Mnuchin said in an 18 January press release.

Instead of tightening regulations the Treasury will work more closely with nonbank financial institutions and try to fix their problems, the press release indicates. Under a new policy adopted in November 2017, the FSOC will analyse institutions’ level of risk and conduct a cost-benefit analysis before taking action.

Efforts to increase the transparency of nonbank institutions’ finances and enhance communication between institutions and the Treasury will be made. The hope is to reduce the cost of compliance and make the process more efficient.

Mnuchin’s action effectively ends the Obama administration’s policy of using regulation to reduce risks from nonbank financial institutions, Reuterspointed out. Instead, Mnuchin and President Donald Trump believe cooperation between government and institutions is a better means of managing risks.

The FSOC was the organization set up to monitor the financial health of large institutions in America after the crisis of 2007-2008. Its task is to identify risks of default or other problems at entities such as banks and insurance companies and take efforts to mitigate that risk. The Treasury Secretary services as chairperson of the FSOC.

The FSOC action is sure to generate controversy because MetLife admitted to “material weakness” in finances on 29 January 2018, Bloomberg Marketsreported. The insurance giant admitted it had not set enough money aside to cover some annuity and pension payments.

Disturbingly, MetLife admitted to losing track of some annuity and pension beneficiaries. Such admissions are an indication of sloppy administration and poor recordkeeping.

MetLife boosted its reserves to $575 million in an attempt cover pension and annuity payments. The company also postponed its earnings call and the date of release for its 4th Quarter 2018 financial numbers to 13 February, for reasons not made clear.

US insurers seriously exposed to pension risks

MetLife is one of a number of American insurers that has taken on serious risks by acquiring pension obligations from American companies, Bloomberg Markets revealed.

The pension obligations MetLife absorbed might include those of the dying retailer Sears Holdings Corporation. Sears revenues fell by 22.22% during 3rd Quarter 2017 and has been selling off assets to cover expenses. Sears may have as many as 20,000 pensioners in the United States.

Retired Sears’ employees might be among those MetLife failed to pay. Such failure to pay can lead to expensive class-action lawsuits in the United States.

News of MetLife’s problems caused the company’s share price to fall from $54.77 on 26 January to $47.04 on 5 February. MetLife, or Metropolitan Life, is a major issuer of Life and other insurance policies in the United States. The company has been trying to raise cash over the past year by selling or spinning off subsidiaries such as Brighthouse Financial.

The problems at MetLife indicate serious structural weaknesses in the US insurance industry that might pose a threat to the American economy and insurance markets. Liquidity problems at another major US insurer, American International Group (AIG), helped trigger the global financial meltdown of 2007 and 2008.

At least other major US insurance company Prudential Financial Inc. is under strict oversight by the FSOC because of its finances, Reuters reported. Prudential is expected to ask for changes to regulations like MetLife did.

Chile, Turkey and Saudi Arabia also follow the slippery slope of debts collection, says Euler Hermes.

Canada and Australia are surprisingly becoming harder places to collect unpaid debts according to new research from trade credit insurer, Euler Hermes.

Euler Hermes provides trade credit insurance that protects companies against non-payments and as such also collects debts on their behalf if the worst case scenario does eventuate. Employing almost 400 debt collectors in 35 different countries, the company has a unique overview of the level of difficulty involved in this process around the world.

The company’s Economic Research department analysed 50 countries and ranked them in their order of being the best to worst places to collect debts as well as the relative change in ease or difficulty involved in debts collection.

The report’s methodology takes into consideration the impact on the complexity of the debt collection process on a country level based on three areas: local insolvency proceedings, local judicial process and local payment practices.

A Collection Complexity Score is then given to each country for the level of complexity for debts collection from 0 (least complex) to 100 (most complex). The score is also split into a four-modality rating system: Notable (score below 40), High (between 40 and 50), Very High (50 to 60) and Severe (above 60).

Saudi Arabia, United Arab Emirates (UAE), Malaysia and China are the most complex countries for debt collection, with respective scores of 94, 81, 78 and 73. All these countries ranked badly because they lack a stable legal framework and their courts independence and reliability is inadequate, amongst many other issues.

Jennifer Baert, Head of Collections at Euler Hermes, said: “In Saudi Arabia and UAE payment terms are quite long. In the UAE it is over 60 days … In UAE we were expecting a lot from the new insolvency law in 2016, but it hasn’t yet delivered on its promise to make debt collection easier.” As reported in the Financial Times

In contrast, countries in Western Europe performed the best with Sweden, Ireland and Germany topping the lead for being the easiest countries where to collect debts.

Amongst the most advanced countries, the US, Canada and Australia surprisingly appear with a ‘Very High’ complexity. The US and Canada score similarity is due particularly to their multi-level system (e.g., county, state and federal structure) in which protection mechanisms are generally impractical, and to the lack of efficiency in recovering an unsecured debt.

The ranking follows a previous report Euler Hermes released four years earlier in 2014. It provides unexpected new insights into the countries improvements or deteriorations over the years.

The country where debt collection has seen the greatest jump in level of complexity is, perhaps surprisingly, Canada. The North American country has seen its complexity score increase by 15.22% to 53.

Besides its multi-level system of government, Canada has few deficiencies. In the event of buyer insolvency, a “Retention of Title” (RoT) clause in a contract can be a powerful tool that protects the seller in retaining ownership of its goods if no full payment has been received.

The Canadian Personal Property Security Act (PPSA) recognises retention of title as a valid means of security. But the issue is its enforcement which is rather uncommon, difficult, and costly.

Australia was next in the list of the biggest percentage deterioration in debt collection complexity, up 8% over four years.

Australian companies pay on time within the typical 30 days average upon receiving an invoice and it is good compared to international standards. However, there was a deteriorating trend in payments and average DSO (Days Sales Outstanding) reaching 60 days.

Late payments issue was hot topic during 2017 that prompted the government to look into it. The Small Business Ombudsman released results of its inquiry into payment behaviour. And this led Prime Minister Malcolm Turnbull to announce that federal government agencies would pay invoices for contracts worth up to A$1 million (£600K) within 20 days, thus slightly reversing the trend.

On the other side of the spectrum, Brazil made the most progress in creating a better debt collection environment over the past four years. The South American giant saw its score drop to 43 from 55, a 21.82% improvement.

Thanks in part to recent modifications to its Federal Law No. 11,101/2005, also known as the Brazilian Bankruptcy and Restructuring Law (BRL), which came into effect in 2005. The enhanced legislation improved creditor protection and the bankruptcy system’s efficiency.

Following Brazil, Slovak Republic, Ireland and Portugal were not far behind with a combined average increase of 18%.

These three countries are members of the European Union (EU) and have strongly benefited from the Union’s various policies. The Late Payment Directive 2011/7/EU was adopted on combating late payment in commercial transactions to protect European businesses, particularly SMEs. The directive constitutes a major attempt to harmonise payment terms across the EU.

The region Europe presents the highest number countries at a ‘Notable’ collection complexity. 14 out of 16 countries stand at the less severe level, the exceptions being Greece and Italy both rated as high level of collection complexity.

Thousands of UK motorists could be driving without insurance because of fraudsters known as “ghost brokers” selling fake insurance policies online, police have warned.

Ghost brokers typically target men in their 20s using social media such as Facebook and Instagram.

City of London Police’s Insurance Fraud Enforcement Department (IFED) warn motorists to ‘Steer Clear of Fraud’ from these mischievous tricksters via its national campaign launched yesterday.

In the last three years, detectives from Action Fraud, the national fraud and cyber reporting, received more than 850 reports of the ghost broking scam that caused individuals and organisations victims losing an estimated total of £631,000.

Millennials, the technology-savvy and always-on social media generation, are the perfect victims who ‘ghost brokers’ often contact on Facebook, Instagram and on many other applications.

They also use other contact methods which include adverts in newspapers and magazines, cold calls and being introduced, either directly or by friends, family members or work colleagues. One specific case is the Portuguese community living around the Epsom and Surrey area where, Renan Gomes, a 33-year-old courier defrauded his victims and insurance company out of a combined £89,000.

Mr Gomes set himself up as an unauthorised insurance broker and sold policies to people who often didn’t speak English. He’s not only threw out of the window his duty of care but also left them with worthless policies.

IFED Detective Constable Eva Woods who investigated the case said: “The warning here is if you get yourself insurance through an unlicensed broker like Gomes, then the likelihood is that you’ll be left without valid cover. You could end up having to foot a hefty bill yourself should you have an accident and you could also have your car seized by police if it’s on the road without valid insurance. Anyone looking for cheap car insurance deals from an insurance broker should make sure that broker is authorised with the FCA (Financial Conduct Authority). ”

A national campaign #SteerClearofFraud has now been launched to warn drivers to watch out for heavily discounted policies on the Internet or cheap insurance prices they are offered directly.

— Insurance Fraud Enforcement Department (@CityPoliceIFED) February 5, 2018

The campaign serves to bring people’s attention to the issue as the police believe that ghost broking is actually being under reported each year due to the way ghost brokers deceive motorists into thinking they have legitimate insurance, when in fact it’s worthless.

They only become aware they don’t have genuine cover when they are stopped by police or attempt to make a claim.

Most people that fall for the scam are young drivers who have seen their car insurance costs going through the roof, recently. According to the Association of British Insurers (ABI), the average cost of motor cover has leapt by 29 percent since 2014.

Young adults just starting as drivers without discount or driving experience face a huge bill that is pushing them to desperately looking for ways to save money on their insurance.

“While an offer of cheap car insurance may seem tempting, falling victim to ghost broking will end up costing you far more in the long run – both in terms of money and your licence.” said IFED Detective Chief Inspector Andy Fyfe.

Five in 10 US households with either homeowners or renters insurance policies are interested in installing smart devices in their home that can detect, prevent damages and notify them or their insurance company in the event of a loss, according to a report from market research firm Parks Associates.

Internet connected light bulbs, locks and kitchen appliances are close to becoming everyday household items. This is, in part because of the widespread adoption of smartphones and tablets, which has created demands for mobile and wireless applications.

The smart homes market, driven by the Internet of Things (IoT) spending, is set to grow 14.6 percent in 2018 to reach over $770 billion (£560 billion) according to a new forecast from the International Data Corporation (IDC). The market intelligence provider predicts that IoT will surpass the $1 trillion mark in 2020 and possibly reaching $1.1 trillion in 2021.

Future will tell if IDC forecasts are right but one thing for sure it that the technology keeps on moving so fast. Last Christmas, all everybody wanted was an Amazon Echo or Google Home. These were the two most popular voice assistant products that can play music, provide information, order a cab, control smart home devices and many other things.

Like telematics in vehicles that benefit insureds with car insurance discounts, navigation and security, IoT is gradually breaking into people’s homes. In fact, home automation technology is not new and has been talked about since the beginning of this century and even before.

In June 2000, BBC Health Correspondent Daniel Sandford reported on a project in which collaborated the charity Dementia Voice, the housing association Housing & Care 21 and the Bath Institute of Medical Engineering to develop a “Smart House” adapted for people with disabilities.

The house, for instance, was supposed to switch off the cooker when the pan boils dry, turn off the bath when left running and even turn the lights on as the residents move through the rooms.

Today, as the Internet takes hold in all aspects of life, many companies are rushing to get in the door by developing smarter home devices powered with the technology. Amazon Echo and Google Home are simply the start of a much bigger future, where millions of households will naturally interact with devices – just by talking to them.

However, there are different motivations and expectations between the generations to what smart homes could offer. Young people tend to be early adopters of new technologies and put emphasis on the media and entertainment (M&E) side compared to their senior counterparts who are more interested in energy efficiency, cost savings and safety.

A connected-home roadmap for the insurance industry then provides many incentives to engage with policyholders to prevent and mitigate risks and collect useful data. This could also help in changing the industry’s poor reputation, probably.

IoT Security and safety

Everyone has the right to feel safe and secure in their home and that’s why security remains the number 1 reason for using smart home systems. Access controls to a property such as IP cameras, video doorbells, doors sensors and other detection systems are hot devices right now.

Neos, a UK startup is challenging the status quo and developing a new product in the insurance market by trying to become the digital guardian – always looking after the things that households value the most.

The company packages IoT devices with home insurance policies; and on signing up insureds receive the devices along with access to a mobile app from which they are able to control all the various installed sensors and connected components. The app is also designed to alert policyholders in the events like a water leak, smoke detected or a front door being left open.

Co-founder and CEO Matt Poll says “The vision really is about moving insurance from [a] traditional claims, payout type solution… to one that’s much more preventative, and technology’s really the enabler for that. We also think that customers get quite a raw deal from their insurance company…for being a really good customer and not claiming.”

Energy management

Increasing costs and demands of energy has led many households to find ways to monitor, control and save energy. Smart meters and Big Data certainly enable insureds to reduce gas and electricity bills, as well as the ability to remotely monitor the systems.

For instance, State Farm insurance partnered with Generac Power Systems to offer its customers discounts on a home backup generator in case of a power interruption.

Likewise, a Canadian company named Ecobee is on a mission to create smarter Wi-Fi thermostats that manage room temperatures with clever sensors. The new devices come with built-in Amazon Alexa voice service that can even order groceries, read the news and much more.

Media and entertainment

As the trend confirms, traditional TV viewership continues to fall among every major demographics due to fierce competition from gaming, online streaming and social media. More and more people are shifting their time away from TV and instead opting for services such as YouTube, Netflix and Amazon, which allow them to watch what they want at any time.

Gaming is also becoming bigger by the day and smashing records. Activision’s latest release Call of Duty: WWII surpassed $1 billion in worldwide sales last year. The franchise is a multiplayer online shooting game set during World War II in Europe, as its name indicates.

Data and cyber risk

The proliferation in the number of devices becoming Internet connected is boosting the smart homes of the future towards a reality. Though, smart homes rely on data, and as data becomes more valuable, insurers will have to rethink new products in order to help protect the stored data against potential cyber risks.

Finally and as Parks Associates suggests home policyholders are open to the range of devices entering their homes only if it helps mitigate risks and provides benefits to the households’ convenience and wellbeing.

Insurers will have to find ways to address cybersecurity vulnerabilities in smart home systems as well as partnering up with hardware and software designers to develop products that offer real value to policyholders, while reaping potential gains for themselves and their partner organisations.

The connected home represents an enormous opportunity for insurers

Separatism has emerged as one of the greatest threats to economic and political stability in today’s world. Catalonia, the region around Barcelona, is threatening to derail Spain’s economic recovery by breaking away after a large number of its citizens voted for independence.

A referendum called by the region’s separatist government on 1 October, but ruled illegal by the country’s central government, had led to Spain’s senate voting on dismissing the Catalonian government and reinstating central control over the region’s affairs. Less than an hour before the vote was due to take place in Madrid, a motion was passed in Barcelona that essentially declared independence and initiated a secession process.

Shortly after, the senate’s vote also passed in Madrid, triggering Article 155 of Spain’s constitution, imposing direct rule and officially disbanding Catalonia’s regional government. Carles Puigdemont, Catalonia’s deposed president, travelled to Brussels to lobby European leaders while 8 of his former ministers were arrested pending potential charges for sedition, rebellion and misuse of public funds.

An arrest warrant was also issued for Puigdemont, who voluntarily surrendered himself to Belgian authorities before being released, pending the decision on an extradition request submitted by Spain.

Madrid has since tried to tread the fine line between zero-tolerance on the Catalonian threat to Spain’s continued unity, and avoiding the kind of clumsy heavy-handed approach that would likely enflame the situation. New regional elections have been called for 21 December to the form a new semi-autonomy Catalonian government.

However, it is feared that the turmoil and political uncertainty provoked by events of the past several weeks will have a serious impact on Spain’s economy over the year ahead, possibly longer if political unrest in the region continues. With a pre-financial crisis economy heavily reliant on the construction industry, Spain was worse affected than most when the world financial systems broke down in 2008. However, after several years in the doldrums, the economy has been staging a strong recovery delivering impressive GDP (Gross Domestic Product) growth for the past three years.

Spain’s Finance Minister Luis de Guindos fears that progress may be impeded. “For 2018, we expect growth of 2.3 percent, which would be 2.7 or 2.8 percent without the Catalan issue,” he told reporters as he arrived at a meeting with his EU counterparts, Reutersreported.

Catalonia is one of the most productive and largest regions in Spain, representing one-fifth of its total GDP. So, any major disruptions will have a significant knock-on effect on the country’s economic performance.

In context, Catalonia attracts 23.8% of all of the tourists visiting Spain and has a lower unemployment with a jobless rate of 13.2% compared to the national average of 17.2%.

In addition, with only 16% of the country’s population, the region manages to pull almost a third of the total new inward investments and exporting more than 25% of the national total.

Among Spain’s 17 regions, Catalonia’s 2016 GDP per capita of €28,590 is surpassed only by the Basque Country’s (another agitator for secession) €31,805 and Madrid’s €32,723. Catalonia also has a lower degree of income inequality compared to other areas of Spain, a factor that contributes significantly towards Catalonians feeling generally wealthier than the population of other regions.

Catalonia’s economic importance to Spain is, ironically, also the source from which the independence movement draws much of its strength. Historically, Catalonia has been the industrial heartland of Spain. Its economy was founded on maritime prowess and the related development of a thriving hub of trade and commerce in textiles and other goods. That has subsequently evolved into a diverse modern economy with the tourism, finance, services and tech industries all thriving.

Fira Barcelona – Mobile World Congress 2017

The industrial history of Catalonia from which the modern economy has evolved can be credited with providing the foundations for its evenly dispersed wealth. It is also likely why the region’s politics have traditionally seen the left have a far stronger influence than in Spain’s other wealthier regions. The coalition of Catalan nationalist parties that formed the government of former-President Puigdemont, while also including conservative representation, are predominantly of a leftist nature.

Until the War of the Spanish Succession lead to the formation of modern Spain between 1713 and 1715, Catalonia was an independent region with its own language, customs and laws. It was though linked with Aragon from the twelfth century by the marriage between Petronilia, Queen of Aragon and Ramon Berenguer IV, Count of Barcelona which united the crowns of the two regions. However, Catalonia was rarely a willing participant in the united Spain and a succession of Kings struggled to impose Spanish language and laws in the region.

In 1931, Catalonia was again granted semi-autonomy within Spain with the establishment of a regional government. That, however, was short-lived with General Franco taking exception to Catalan separatism, marching on the region and winning back control with victory at the Battle of Ebro in 7 years later in 1938. When democracy returned to Spain in 1977, Catalonia was again granted semi-autonomy and up until the financial crisis Catalans seemed reasonably content and enjoyed a peaceful dual identity as both Spanish and Catalonian.

Spain’s economic woes following the international financial crisis provided a new platform for Catalan’s nationalist parties to gather popular support on the ticket that the region’s stronger economy was propping up much of the rest of the country. Despite a wider recovery over the past few years, that momentum has built, eventually culminating in last month’s events. With it clear that Madrid, and Europe, will do everything in their power to prevent Catalonia’s secession (independence would almost certainly trigger similar movements in the Basque country and across Europe) the question is now how to build bridges and mend fences.

Hope lies in the fact that it is still believed that a majority of Catalans would prefer to find a solution that does not involve full independence. While 90% of voters who turned out for the illegal referendum voted in favour of independence, overall turnout was only 42%. Those in favour of remaining as part of Spain are thought to account for the vast majority of the remaining 58%.

The reaction of Catalonia-based business also suggests that the local economy would also be far less successful as an independent nation. Reports, admittedly Spanish government reports, suggest that more than 2,000 Catalonia-based firms decided to leave the region following the referendum vote. The two largest banks in the region, CaixaBank and Sabadell were at the vanguard of the exit amid reports the uncertainty was have a negative effect on deposits.

The Chief Executive of Freixenet, a Cava maker strongly identified as Catalonian, indicated the company is also considering its position by stating “businesses need legal certainty and we do not have it right now.”

It is clear that much relies on next month’s elections and the hope that a new Catalonian government can negotiate terms that will lead to an amicable solution to the secession argument. Catalonian independence would undoubtedly inflict a deep wound on Spain’s economy but the region itself would also suffer hugely. There would be no likelihood of the EU accepting an independent Catalonia into the fold in the foreseeable future as doing so would set a precedent for every region in Europe with political parties holding similar aspirations.

How Catalonia’s economy might bounce back in the longer term is impossible to predict but it would certainly be a painful adjustment in the shorter and medium terms.

With so much at stake on both sides, the chances are that a new government will negotiate concessions such as greater financial autonomy for the region and possibly recognition as a ‘nation’ within Spain. In the meanwhile, the uncertainty has already knocked at least a few percentage points from Spain’s GDP growth for 2018 and the situation needs to be resolved with expediency.

Insurers are set to profit from the recent Saudi Arabia announcement to end a longstanding royal policy that prohibited women from obtaining licenses, and hence driving. The change will take effect in June 2018.

The lifting of the driving ban for women is likely to improve a number of sectors within the country’s economy, from car sales to insurance, besides giving a huge boost to its reputation.

Indeed, the decree is to impact the lives of more than 8 million women over the legal age to drive, including foreign women living in Saudi Arabia. This will also encourage more women to join the workforce resulting in productivity gains for the economy.

The decision is part of the country’s new political direction towards an economy less reliant on oil. The goal is to transform the kingdom into a global investment powerhouse with an ambitious project branded as Vision 2030

Insurers, retailers and car companies are the major winners from this lifting of the ban. It will also comfort investors, especially foreign investors, that Saudi Arabia has the political will to become the growth engine of the Middle East.

Saudi Arabia insurance market

The insurance market in Saudi Arabia is still considered as an emerging market. In 2016, the total revenue or gross written premiums (GWP) reached USD $9.9 billion, which represents less than 1 percent share of the total world premiums. However, the country has recorded high growth rates during the last five years thanks to enforcements of compulsory insurance, population growth, the increasing number of workers and vehicles and an improved insurance awareness among other things.

According to latest reports from the Saudi Arabian Monetary Authority (SAMA), over 7.3 million insurance policies were sold in 2016, compared to more than 8 million in 2015. The small drop reflects turbulences the kingdom is going through as a result of an unpredictable power-play between the new and old generation’s vision for the kingdom.

Nonetheless, Saudi Arabia’s insurance sector is a stable and regulated market. SAMA introduced a number of regulations covering areas such as risk and compliance management, fraud and anti-money laundering and solvency requirements. These regulations have helped shape the domestic insurance sector.

The majority of the direct insurance business is in health and motor insurance. This was served by the top three companies in the country namely Tawuniya, followed by Bupa Arabia and MedGulf. In total, there are 35 licensed insurance and reinsurance companies listed in the Saudi Stock Exchange, aka Tadawul.

Motor insurance market

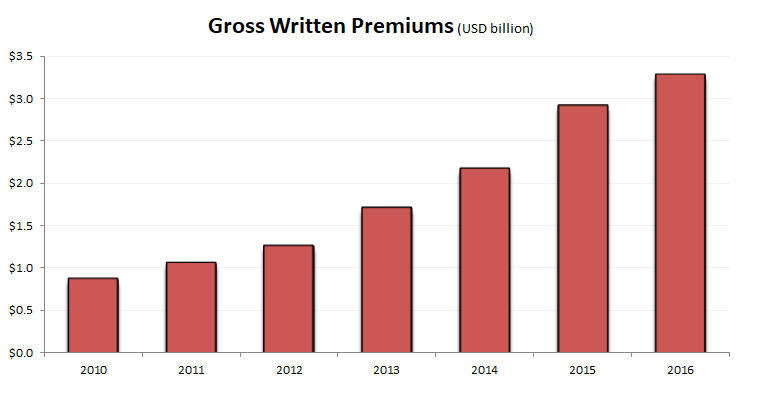

Motor Insurance is the second largest segment in the Saudi insurance market and represents 33% of the overall gross premiums written in 2016.

The sector totalled USD $3.3 billion and recorded an average annual growth rate of 20 percent since 2010.

Saudi Arabia motor insurance gross written premiums growth 2010-2016

The kingdom exceptional growth appears as a tantalising prospect of increased opportunities for insurers. However, some of the growth is due to regulations introduced by kingdom’s financial authority.

Saudi roads are among the most dangerous in the world. Over 9,000 people were killed in car accidents in 2016, making it the highest in the region. The government has been working hard using technology along with the insurance industry to reverse the trend. This had few successes when the General Department of Traffic (GDT) introduced Saher, an automated traffic control and management system that monitors traffic in real time and tracks violations and accidents throughout the kingdom.

But one of the insurance industry’s most important contributions to road safety has been the establishment of Najm Insurance Services. The company assists drivers in the immediate aftermath of an accident by evaluating damages, helping to file accident reports and serving as a liaison between policyholders, the authorities and insurance companies.

In recent years, the Saudi motor insurance sector has seen an increase in market concentration and is currently dominated by three companies namely Malath insurance, Al Rajhi Takaful and Tawuniya having market share of more than 40% collectively.

Lifting of the ban impacts

Many studies have been conducted over the years to determine whether women are safer drivers or not. And most of these studies have confirmed that women take less risk while behind the wheels.

This is probably what the Saudi Interior Minister, Prince Abdulaziz bin Saud bin Naif, was thinking when he twitted that “Women driving cars will transform traffic safety to educational practice which will reduce human and economic losses caused by accidents,”.

By allowing women to drive, the kingdom could potentially increase its very low female labour force participation rate and therefore boosting the country’s economic growth. More women participation produces more cars on the roads and therefore more insurance policies written.

“The number of cars in Saudi Arabia is likely to increase at least 20 percent in the next ten years as a result of the decision,” said Jaap Meijer, the head of research at Dubai-based investment bank Arqaam Capital, Bloomberg reported.

In any case, the Saudi Arabia insurance industry welcomed the move and looks forward to working with all parties in growing and improving the market.

French insurer AXA launches new flight delay insurance product based on the latest Blockchain technology that offers automatic compensation to travellers who have their flight delayed by more than 2 hours.

The roll out of its new insurance product, wittily named Fizzy, makes the insurer a pioneer in the insurance industry to adopt Blockchain. The technology, behind the success of the digital currency Bitcoin, has gained significant popularity and is now assumed to be the next big technological disruption.

Since setting up AXA Strategic Ventures, a $275M venture capital fund dedicated to investing in emerging innovations, the company has been spending a tremendous amount of money in the InsurTech (Insurance Technology).

With Fizzy, AXA is capitalizing on its first-mover advantage to showcase its abilities to adopt and develop real world applications based on the new technology.

One of the tenets of insurance is to provide ‘peace of mind’ and financial security, which AXA has been successful at providing so far. However, the industry is still plagued with a negative reputation for ‘trust’. By using the public Ethereum Blockchain, AXA wants to restore that trust since transactions on the Blockchain network are transparent and therefore available to anyone to verify.

“Building customer-oriented offers is our definite goal at AXA. By removing insurance exclusions and using an Ethereum smart contract to trigger indemnifications, we increase the level of trust our customers can have with AXA,” said Jean-Baptiste Mounier, Media Relations Officer at AXA, to CoinDesk.

How Fizzy works

Fizzy is pitched as a smart insurance and automatic compensation platform and it is available at Fizzy.axa. The application provides a streamlined and instant compensation process without requiring policyholders to submit a claim. It is done automatically and the decision is delegated to an independent network.

Up to 15 days prior to departure of their booked flights, customers can purchase insurance coverage on Fizzy by filling out their personal information and flight ticket details.

The data is then stored on the tamper-proof network, the Ethereum blockchain, and used by self-executing computer programs, aka smart contracts, connected to global air traffic databases that constantly monitor flight data. When a flight delay of more than 2 hours is detected, Fizzy informs the policyholder immediately and triggers the compensation payment.

For the time being, all Fizzy payouts are made in government-issued currencies. However, in the future AXA envisages denominating those payments in Ether (ETH), the unit of cryptocurrency used on the Ethereum network.

Along with Ether, AXA’s immediate goal is to expand the solution internationally and develop partnerships with airline companies, travel agencies and airports to further improve users’ travel experience. Right now, Fizzy is in beta (test phase) and covers only direct flights between Paris Charles de Gaulle airport and the United States, in either direction.

The transactional data captured during the test phase will allow AXA to pick up any issues with the platform and to lay out the foundation for system-wise scalability that sustains its future operational growth.

Fizzy will be handling a massive amount of data since the solution is offered as a no exclusion insurance product which means that compensation is paid to policyholders’ when their plane is late for any reasons: weather, strikes, plane mechanical issues, airport computer failure and even alien attacks.

Flight delay insurance

Air travel insurance has evolved since the first 1950s package holidays in the UK and it has now reached a multi-billion market worldwide. Unfortunately, flight delays are, amongst other things, part of the aviation operations. The US Bureau of Transportation Statistics makes flights data freely available that shows the magnitude of the problem.

In the last 10 years, on average 20 percent of all frights in the US were delayed as shown in the Bureau’s On-Time Performance data below

US Bureau of Transportation Statistics – Flights On-Time Performance

Flight delays are an inconvenience to passengers and can cause many problems such as missing a connection, lost business opportunities, missing interviews or meetings and much more.

However, sometimes the airline is not at fault and the reasons are outside its controls. The top causes of delays recorded by the US Bureau were aircrafts arriving late, national aviation computer system, airline operations management issues, extreme weather and security.

Bureau of Transportation Statistics – Delay causes by year

In Europe, there were nearly 120,000 flights delayed and over 7,000 cancelled in just last October month according to estimations from Flight Global statistics. Under European regulations, a delay of two hours or more for flights of 1,500 kilometres (930 miles) or less puts the onus on the airlines to offer passengers assistance with free meals and refreshments as well as means of communications to make phone calls or send emails.

The regulations spurred the airlines to improve performance and prevent delays but there are still many flight delays occurring.

Blockchain goes mainstream

Although AXA is the first major financial institution to adopt Blockchain, disrupting the insurance space and coming up with innovative solutions using the technology is not new. Many startups have successfully established new products and others are still trying to figuring out a business model.

The earliest individuals willing to tackle the flight delays problem was a team called InsurETH that built a flight insurance product on the Ethereum network at the London FinTech Week Blockchain Hackathon in 2015. The InsurETH team even won a prize for their prototype but unfortunately it seems that the project is not going anywhere further.

A startup named Etherisc picked up the slack last year and claims to have developed the first decentralized insurance application, Flight Delay Dapp, which can issue policies and pay out valid claims completely autonomously.

“The frustration of a flight delay or cancellation is a familiar feeling for many travelers – and an unpleasant experience that is often compounded by having to deal with traditional insurance,” said Stephan Karpischek, Etherisc’s co-founder and CEO, as reported on Blockchain News.

Blockchain and smart contracts will definitely impact the insurance industry because it offers many benefits such as the potential to fully automate the claims processing and thus lowering operating costs, as well as transparency since all data is publicly auditable and can be freely analysed by third parties. However, there are also many challenges for blockchain mainstream adoption such as security (more people on the network, more entry points and more hacking vulnerabilities), scalability of the network and most importantly the legal issues.

Therefore, the insurance industry will need to work with the regulators to review, reinterpret and perhaps change a number of areas of the law in order to spur Blockchain-based insurance products to take off.

The greatest danger from massive cyberattacks like the Equifax hack is “data breach fatigue.”

Data breach fatigue occurs when people simply stop paying attention to news about cyberattacks. This occurs for several reasons including boredom, bad news reporting, over-reporting of cyberattacks, lack of knowledge, and media hype that distorts or overstates the scope of such attacks.

There was strong evidence that the public was becoming desensitized to reports about data breaches two years ago in 2015. The Invincea Endpoint Security blog noted that the public was becoming “Anesthetized by Data Breaches” as early as 26 June 2015.

The situation has gotten far worse with all the news about massive cyberattacks such as the latest one on Equifax, the giant American credit-reporting firm. Consumers “tune out” news reports about such attacks because they are often inaccurate or sensational.

They also learn to ignore constant news reports about such attacks, especially when it does not pertain directly to them. Many Britons will ignore news about the Equifax breach because it occurred in America, for example.

Data breach fatigue helping cybercriminals

A greater problem is that cybercrimes utilizing stolen data rarely occur immediately. Crooks may wait for weeks, months, or even longer to use the data.

Cybercriminals understand that many people and organizations will let down their guard as breaches fade from the news cycle. Some predators might even try to encourage data breach fatigue by deliberately waiting to use their stolen information.

These circumstances make data breach fatigue a major risk that insurers will have to take into account when writing policies dealing with identity theft or data. Data breach fatigue is particularly destructive because it can mitigate many security measures such as employee education, and password protocols.

People most at risk

An early step will be to identify those individuals and organizations most at risk from data breach fatigue.

Smaller firms and organizations, where data management and IT are not a core activity, will have a greater level of risk. A danger at smaller firms can be the lack of dedicated security personnel and regular training.

Manufacturers, shippers, retailers, and other companies that make extensive use of information technology but have no specialty in it have a greater risk. Particularly prone to data breach fatigue will be employees that need to use databases as part of their job but do not specialize in IT.

Such individuals can include salespeople, factory workers, drivers, managers, cashiers, sales clerks, accountants, loan officers, traders, bankers, customer-service personnel, file clerks, and even attorneys. A person with a hectic schedule will be far more likely to ignore security protocols. So will people who need quick access to financial data but have limited computer knowledge.

The risk from data breach fatigue is exploding because of the growing use of smartphones and other mobile devices to access financial data. A busy salesperson’s phone might contain bank account or credit-card numbers for dozens of customers – yet have only standard encryption.

Mitigating the risk

The most effective means of mitigating data breach fatigue will be to accept it as a fact of life.

The most insidious aspect of data breach fatigue is that everyone is susceptible to it. Complacency and arrogance are the greatest threats. Most people overestimate their ability to follow security protocols and underestimate criminals’ ability to penetrate defences.

Compliance with security protocols usually drops off as news about a major breach fades from the public attention. Complacency often grows lax because the massive losses predicted by news articles do not occur, leading many people to falsely assume that cybercrime is nothing but media hype.

No amount of education or oversight will eliminate data breach fatigue because it is rooted in human nature. Most people are simply incapable of a regular focus on data security.

Technological solutions to breaches

Instead, the real solution will be in the reconfiguration of databases, security software, and other applications to cope with data breach fatigues. Programmers and engineers must design systems that automatically compensate for data breach fatigue.

An excellent example of a safeguard against data breach fatigue is a system that automatically requires users to update their passwords on a regular basis. Another good defence is a system that asks a security question on a regular basis. Such protocols have become commonplace on financial-services and insurance websites in America.

Greater layers of security are possible even on websites and systems used by the general public. A popular solution that is being widely used by Amazon and other companies automatically texts a randomly-generated code or password to a users’ phone.

Such technological fixes are the best mitigation for data breach fatigue because they eliminate the human factor. Instead, the system itself forces compliance with security protocols and requires users to update data on a regular basis.