Financial institutions are at greater risk for money laundering losses than ever before. The Danske Bank scandal reveals that even institutions in law-abiding nations have a high risk of money laundering losses.

For example, launderers reportedly used 15,000 accounts at Denmark’s largest bank for suspicious transactions. Disturbingly, the suspicious activity at Danske Bank’s Estonian branch went on for nine years from 2007 to 2015. Tellingly, Danske Bank made that revelation in a press release.

The suspicious transactions involved €200 billion ($235 billion). In particular, investigators labelled the “vast majority” of 6,200 Danske Bank customers in Estonia suspicious.

Lax Anti-Money Laundering procedures

“Danske Bank has previously concluded that it was not sufficiently effective in preventing the branch in Estonia from being used for money laundering in the period from 2007 to 2015,” the bank itself admits.

Lax Anti-Money Laundering (AML) procedures and limited enforcement of AML laws created the risks at Danske Bank, CNN Money reports. “Fragmented and inconsistent” regulation makes money laundering easy in Europe despite strict EU AML laws.

All launderers need to do to evade AML is put money into one bank account in any EU country. Launderers target lesser institutions, like Danske Bank in smaller countries like Estonia, because of weak AML regulations.

Risks from AML Failures are growing

The risks from AML failures are growing dramatically because penalties for money laundering are increasing.

For example, Denmark’s parliament increased fines for AML violations by 80%, The Guardianreported. Significantly, Danske Bank is already facing a £475 million fine in Denmark.

The European Union is expanding its definition of money laundering, Global Compliance Newsreports. For instance, the latest Anti Money Laundering Directive (AMLD) covers digital wallets, prepaid cards, cryptocurrencies, digital wallets, and art as well as bank accounts.

Therefore, the EU could prosecute cryptocurrency exchanges, digital wallet operators, issuers of prepaid cards, and even art dealers for AML violations. For example, it could prosecute Apple if launderers moved money through Apple Pay.

The AMLD creates new markets for AML insurance products. Providers of cryptocurrencies, digital wallets, e-commerce platforms, and even comic-book or art dealers might require AML insurance or bonding.

The EU is promising to increase the powers and capabilities of Financial Intelligence Units (FIUs) to better enforce AML laws. The FIUs are law enforcement units set up specifically to fight money laundering.

How AML is changing banking

AML regulations are dramatically changing banking. The latest AMLD eliminates anonymity for bank accounts and safety deposits in EU countries.

The same directive requires banks to report information on real estate owners to authorities. The same AMLD makes ownership details of EU-based companies’ publicly available information.

The AMLD could lower risks for insurers by requiring AML due diligence at financial institutions. In particular, the EU could require enhanced AML due diligence on transactions from “high-risk” countries.

They do not identify the high-risk countries, but the EU is preparing a list of nations that are “politically exposed to corruption,” Global Compliance News reports. Presumably that means countries with high-levels of corruption or money laundering.

It will require enhanced AML due diligence for transactions from high-risk countries. Under the regulations, EU members may require greater AML measures. It will allow only transactions from countries or institutions that comply with EU AML laws.

How Money Laundering threatens Insurers

The Danske Bank scandal proves that money laundering and AML are becoming grave risks to financial institutions. Insurers had better take notice because it will target them for AML enforcement at some point.

An obvious way to head off such enforcement will be to apply AML measures to all claims and premium payments. That would reduce the risk of launderers using insurance policies to get around AML laws.

A launderer could buy an insurance policy on a vehicle and deliberately crash it to generate a claim, for example. Such fraud is likely if the EU AML crackdown is successful.

Performing AML due diligence on clients and policies from high-risk nations could reduce the risk of such fraud. Stronger AML enforcement will force launderers to find new ways to move money.

The Danske Bank scandal shows how money laundering creates risks and opportunities for the insurance industry. Insurers that understand AML can avoid losses and exploit new opportunities created by money laundering.

More and more people are turning to technology to help them make positive strides in getting better ways to access care and benefit from simpler healthcare experience.

This upsurge in consumer demand for digital-based health services is creating a new model for care in which patients and machines are joining doctors as part of the healthcare delivery team, according to results of a survey from Accenture.

The Meet Today’s Healthcare Team: Patients + Doctors + Machines report surveyed almost 8,000 people across seven countries to assess the rates of adoption for health-related technology and people’s attitudes towards sharing electronic health records (EHRs).

Unsurprisingly, the adoption rate for health-related technology is increasing across the board with the exception of health-related website use which seems relatively steady. Technologies, ranging from mobile apps to smart scales to wearables have seen significant growth in the past few years with no sign that this growth will slow.

And wearables are not simply ways to gather data and to monitor health.

Wearables also encourage healthy behaviours through subtle nudges such as a vibration to remind you to move after periods of inactivity or gamification and competition on data-sharing sites. Some products can even warn of impending cardiac arrest.

The survey found that the number of people willing to share EHRs is also increasing. However, there is a clear preference towards sharing data with a doctor, medical practitioner or family member whereas sharing data with their employer or a government agency was treated with more suspicion. Use of wearables in the workplace to monitor employee efficiency may further heighten this suspicion.

Artificial Intelligence (AI) – which offers significant benefits for both the wearer and the healthcare provider – seemed to split respondents with just under half expressing a positive view of the benefits of AI when it came to interpreting their EHRs.

For insurers, the report highlights two trends of particular interest: the growth of wearable technology rising from 9% in 2014 to 33% in 2018 and the high numbers of respondents willing to share their data with a health insurance provider (72%).

Both trends indicate a growing opportunity for wider integration of technology and wearables with the health insurance which should benefit both the consumer and the insurance provider.

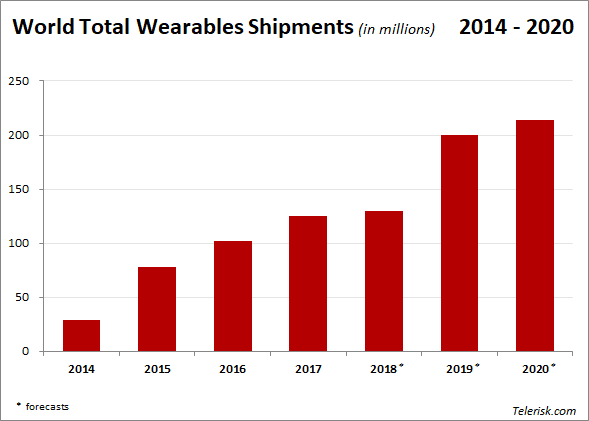

Since the first iterations of wearables in the early 2000s, which were little more than electronic versions of old-fashioned pedometers, the market has exploded.

An estimated 125.5 million devices were shipped in 2017 with forecasts that the market could almost double to 240 million devices by 2021.

Wearables Shipments 2014/2020 – Source: IDC Tracker

This growth of wearables has overlapped significantly with developments in smart watch technology making products like the Apple Watch one of the best-sellers in this category.

Other products are broadening the range of what we would consider health-related wearable. Spire produces a breathing-monitoring device that helps manage stress and Neuroon is an eye mask that promises to improve your sleep. Some firms are even promising clothes with built-in sensors.

The senior “Gold Rush”

Contrary to the assumption that this kind of tech is for younger and active users; a growing selection of wearable products are specifically aimed at seniors.

These ranges from more traditional products which gather and monitor health data to shoes equipped with sensors that sound an alarm if someone falls or check that wearer has moved recently. In these cases, wearables are not only providing healthcare benefits but also quality of life benefits for seniors with increased, or sustained, mobility and independence.

And these products aimed at those aged 55 may be the next area of explosive growth. The trillion dollars market for senior-focussed products is being described as a “gold rush”.

This growth of products aimed at the lucrative seniors’ market would likely lead to even wider adoption of these technologies by the under 55s. Biohackers, for example, are always looking for ways to repurpose medical technology to gain an edge. In turn, these innovations are often what spark wider consumer adoption creating a cycle of adoption and innovation.

With wide adoption of external, surgically implanted external blood glucose sensors and recent FDA (Food and Drug Administration) approval for blood glucose implants in the US, implants are likely to be the next iteration of these advancements. One clinical study described the widespread adoption these as imminent: “perhaps even in the next decade.”

Opportunities for health insurers

In addition to investments in the technology aspects of this market, the growing overlap of technology and healthcare has attracted the attention of the health insurance market.

A recent CapGemini report forecasts that “wearables will impact all parts of the insurance customer journey” through personalized products, continuous underwriting, policyholder service & risk control and claims management.

Some of these ideas are not new and traditional insurers saw the benefits of wearables relatively early. Early partnerships with firms such as Fitbit offered incentives and discounts based on the user’s level of activity.

However, the effectiveness and benefits of these initiatives are unclear as the data collected was minimal and often shared via the employer, something users were reluctant to do as Accenture found.

However, with thousands of healthtech startups and devices producing significantly richer sets of EHR data, there are growing opportunities to integrate wearables into health insurance.

Mountain View, California’s HealthIQ is offering fitness-oriented individuals more favourable insurance plans due to their active and therefore assumedly healthier lifestyles. HealthIQ surveyed over a million people and partnered with medical researchers to support this approach and had over $8 billion in coverage under management in May 2018.

Other startups are offering to coordinate data management between the insurance firm and the user, cutting the employer out of the picture. Australia’s Fitsense is placing itself in the centre of this relationship by providing data analysis and processing to help build individual risk profiles on consumers for use by insurance and healthcare providers.

With such innovations and opportunities, the increasing use of EHRs gathered through wearables by health insurers is set to increase. This offers opportunities for both the consumer with targeted customized coverage, and insurers who can better manage their risks.

However, with insurers potentially holding massive troves of what amounts to users most personal information, the onus will be on insurers and data handling services to protect and manage this data carefully.

A data loss, or worse a data compromise, would significantly erode the confidence of users and likely stifle this opportunity for integration.

Climate Change is dramatically transforming the insurance industry. The troubled Aspen Insurance Holdings reportedly agreed to sell itself to private-equity giant Apollo Global Management LLC for $42.75 a share.

California wildfires, widely blamed on global warming, caused a $135 million (£100 million) underwriting loss at Aspen in 4th Quarter 2017, Artemisreported. Aspen is probably facing even greater losses from this summer’s California wildfires, which were apparently more destructive.

Fires and other climate-related catastrophes devastated Aspen’s reinsurance business last year. Observers blamed climate related disasters for 55% of the company’s losses in 3rd Quarter 2017, and 75% of the 4th Quarter 2017 losses.

Wildfires are not the only climate catastrophe affecting insurers. According to Insurance Business Magazine, Aspen took heavy losses from hurricanes Maria, Irma, and Harvey in 2017. The Magazine estimated Aspen’s pre-tax losses for the first three quarters of 2017 at $310 million. News reports did not specify hurricane loss amounts.

Aspen CEO Stephen Postlewhite resigned on 26 January 2018; a day after the company revealed the underwriting losses, Business Insurancereported. Disturbingly, Aspen admitted actual 2017 losses could be greater.

Private Equity profiting from Climate Change

Aspen’s problems were Apollo Global’s opportunity. The private equity fund will pay $2.6 billion for Apollo’s $12.9 billion in assets.

Apollo is one of several private funds shopping for insurance assets. Bain Capital Private Equity paid £1.2 billion ($1.5 billion) for Esure Group LLC in August. Cinven Ltd is reportedly in talks to acquire one of AXA SA’s retirement products units, Bloomberg claimed.

Private equity funds are buying insurers to gain the float generated by insurance premiums. Float is a stream of revenue that an investor can tap to make acquisitions or pay debt.

The strategy of using float to finance equity investments is a speciality of American investment legend Warren Buffett. Buffett used float from the auto insurer GEICO, and reinsurance operations, to build his Berkshire Hathaway empire.

Equity operators like Apollo Global’s Leon Black are trying to emulate Buffett by buying up troubled insurers. By purchasing Aspen, Apollo gains access to premiums from annuity provider Athene Holding Ltd and reinsurer Catalina Holdings Bermuda Ltd.

Aspen Insurance will go private in 2019

Insiders expect the Aspen-Apollo deal to close during the first half of 2019, Reuters reported. After the deal, Apollo will become a privately held portfolio company owned by Apollo Funds. Aspen’s board still needs to approve the acquisition.

Aspen Insurance Holdings has operations in the United States, the United Kingdom, Canada, the United Arab Emirates, Singapore, Ireland, and Australia. Its current headquarters location is in Hamilton, Bermuda.

Aspen Insurance Holdings trades on the New York Stock Exchange under the ticker symbol AHL. Aspen Holdings had a market capitalization of $2.455 billion and a share price of $41.12 on 31 August 2018.

Aspen reported a $14.8 million loss at the end of 2nd Quarter 2018. Stockrow data shows Aspen’s revenues declined by 13.07% during 2nd Quarter 2018.

Insurers facing tough times ahead

Scientists believe shifting weather patterns created by Climate Change caused by greenhouse gases caused California’s wildfires. Climate Change leads to high temperatures which makes the fire season worse.

“The weather patterns are just stuck,” Jennifer Francis a Professor at Rutgers University said. “They’re trapped.” Francis is an expert in atmospheric circulation.

Fires have taken a terrible toll on California this summer. The Chronicle estimated that wildfires destroyed over 1,000 homes and killed eight people by 3 August 2018.

The peak fire season in the Western United States is now nine days longer than it was in 2000, a study by Columbia University and the University of Idaho found. Insurers can expect increased fire risk around the world, Francis predicted.

“We’re seeing this mix of conditions across North America and Europe, but they’re all connected,” Francis said. Under those conditions, high underwriting losses might be the new normal for many insurers.

Interestingly, publicly held insurance companies might be one of Climate Change’s first casualties. Other publicly traded insurers are likely to follow Aspen’s lead and sell out to privately equity firms to cover underwriting losses.

Hacks of cryptocurrency exchanges in the first half of 2018 led to losses of over $770 million (£594 million) highlighting the continued vulnerability of these platforms, which need to find imperatives to establish trust with their customers and the future of the technology.

Despite the underlying security of many of the currencies themselves, investors are learning painful lessons when it comes to the stability and security of exchanges and the associated tools and services.

Exchanges and digital wallets for the storage and transfer of cryptocurrencies quickly sprang up following the release of Bitcoin in 2009, but users were faced with three significant challenges from the outset: malicious attacks, technical shortfalls and fraud.

As Bitcoin approaches its 10th birthday, recent losses highlight that these three issues remain unresolved, starkly underlined by Japanese exchange Coincheck $535 million loss in January 2018.

2018 echoes 2014

January’s hack of the Coincheck exchange was the biggest exchange loss since the $450 million hack of the MT. Gox exchange in 2014.

Despite the intervening years, Coincheck and other significant losses in 2018 highlight how fundamental weaknesses in exchanges and wallets have yet to be overcome. By July 2018, major cryptocurrency losses from exchanges exceeded $770 million.

Coincheck set a bad precedent for 2018 when initial reports of $400 million in NEM tokens being stolen surfaced in January. The company eventually estimated that tokens valued at $535 million had been illicitly transferred from the system leading to the platforms, eventually suspending trading for all currencies apart from Bitcoin.

Two hacks in South Korea rounded out the first half of the year when the Bithumb and Coinrail exchanges were both hacked in June with total losses of $72million (£54m).

But these figures are only part of the picture: smaller losses, like the $3.3 million lost from Indian exchange Coinsecure, push actual losses significantly higher than the estimated $770 million highlighted.

And this trend looks set to continue in the second half of the year. In July, Israeli exchange Bancor reporting a loss of $24 million; so, losses for 2018 could easily top $1 billion by year’s end.

However, with Bitcoin’s 10th anniversary approaching, it is reasonable to wonder why, after a relatively long time in digital years, exchanges and associated technologies like digital wallets, appear to remain so vulnerable.

In many ways, the technical, decentralised nature of cryptocurrencies may explain why overcoming these challenges is and will be difficult. While improved security and better regulation may have helped avoid or limit many of the hacks outlined above, these concepts are largely anathema to the libertarian philosophy underpinning cryptocurrencies.

Improve exchanges security

The original Bitcoin white paper and earlier cryptocurrency concepts proposed by people like Nick Szabo, put security and verification of transactions at the heart of the system.

Blockchain, the foundation of this protection, has since transformed into its own ‘hot’ tech sector even drawing in unlikely players like the Long Island Iced Tea Corporation.

However, despite the security precautions baked into the more reputable currencies themselves, exchanges and digital wallets remain vulnerable due to a range of lax security measures.

These weaknesses range from poorly constructed codebases to single points of failure which thwart other security measures that are in place. For example, the MT. Gox exchange was riddled with security weaknesses from a poorly constructed and loosely managed codebase to loopholes in transaction management, the flaw which allowed hackers to make off with $450 million.

Meanwhile, attempts to improve the security of exchanges have been at best sloppy or at worst, deliberately misleading. The Bitfinex exchange was reportedly secured by multi-sign wallets, similar to a physical safe which required two of three different keys to open.

However, this system was easily circumvented by hackers who discovered that instead of three separate keys in different locations, two keys were stored in a ‘hot wallet’ on the Bitfinex servers. With access to a hot wallet – one accessible via the internet unlike an offline ‘cold’ wallet – hackers easily accessed two keys via a single exploitation. After this, triggering illegal withdrawals was relatively straightforward.

While there may well be outright fraud in the system, security weaknesses generally seem to stem from two issues: The first one, being the Wild West approach to cryptocurrencies, which are grounded in a mistrust of central regulators.

While the reputable currencies themselves adhere to strict rules and controls, other currencies, exchanges and tools like digital wallets, attract groups and individuals looking to make a quick buck: groups for whom security is almost an afterthought.

This is starkly illustrated by the lax approach many exchanges have to basic IT security measures.

Of the 35 organizations surveyed by Dashlane recently, 70% were found to have basic security flaws in their password management systems. Some allowing passwords as basic as ‘1234’ or simply ‘a’ leaving user’s accounts “perilously exposed” according to the report.

Passwords are only one facet of online security but Dashlane’s report noted that:

“For an industry that prides itself in its cybersecurity innovations, the cryptocurrency exchanges are much weaker when it comes to password security than the average mainstream website.”

Given how frequently password vulnerabilities are the root cause of hacks, this weakness is alarming. Moreover, this lax attitude to passwords likely reflects the overall attitude to security.

The second issue is the complexity of cryptocurrencies and the associated technologies.

Cryptocurrencies owe more to cryptography and advanced math than basic computer science. Layered onto this is the added difficulty posed when conducting financial transactions meaning that cryptocurrencies are significantly more challenging than other start-up sectors.

While the Bitcoin white paper is elegant in its simplicity, the application of these concepts in practice throws up a series of wicked problems which are hard to solve. This complexity is exacerbated by the shortage of engineers able to tackle these issues meaning that even if there is a willingness to tighten security; exchanges may lack the necessary skills and abilities.

This freewheeling, libertarian mindset and technical complexity is also apparent when it comes to regulating these exchanges.

Faster government regulations response

Born from a distrust of central regulation and fiat currencies, cryptocurrencies are libertarian at heart posing an immediate challenge to the idea of regulation. Moreover, like any online business, moving location is often a relatively straightforward matter of switching servers to a more permissive jurisdiction.

This has meant that attempts to regulate or licence cryptocurrency firms by states like New York have met significant oppositions and, in some cases, led to the departure of firms.

Compared to the relaxed atmosphere of other locations, such as Switzerland’s canton of Zug, jurisdictions with any forms of regulation will find it difficult to compete as a home for these firms.

However, this opposition to regulation is compounded by the sluggishness on the part of governments to regulate these currencies and exchanges.

Japan’s Financial Services Authority (JFSA) released a report after an assessment of 23 firms finding an overall climate of loose business practices and glaring security flaws. But the JFSA has been looking at the stability and reliability of crypto exchanges since the MT. Gox hack in 2014.

This makes Coincheck hack in January all the more startling particularly when Japan possibly accounts for as much as 65% of the major losses identified between 2014 and 2018.

Nobuchika Mori, JFSA Commissioner and architect for much of Japan’s policy on cryptocurrency regulation

However, Japan is not alone in its inactions, nor are financial regulators necessarily lagging their counterparts.

Governments worldwide are struggling to adapt and respond to the disruption caused to traditional industries such as transportation and hotels. When regulation of scooters is a challenge, it is not surprising that dealing with something as complex as cryptocurrencies is time consuming and slow.

Industry-led improvements present an opportunity

Failures on many other disruptive platforms – a shoddy cab ride, bad rental experience or the inconvenience of abandoned scooters – only affect individuals or small groups at a time. Meanwhile, cryptocurrency exchanges service thousands of consumers and hold billions of dollars in tokens making the repercussions of failure much more widespread.

Moreover, lax exchanges with poor security and anonymity also lend themselves to illicit transactions and money laundering.

These twin issues of consumer protection and the darker side of crypto exchanges servicing illegal online activities would suggest that authorities have a pressing responsibility to reign in and regulate this space.

As with all regulation, many will complain about the burden and cost and some may vote with their feet and substitute New York for Zug. But despite their libertarian tendencies, reputable operators who already act responsibility should welcome some forms of regulation and improved security standards.

Self-regulation and cooperation with authorities would reward conscientious firms and close out competition from less reputable actors improving the space for consumers, exchanges and the currencies themselves.

This presents an opportunity for reputable actors to become leaders and dominate the space to the advantage of both themselves and consumers.

Bain Capital snaps up Esure, the insurance firm that owns the Sheilas’ Wheels brand, in a £1.2bn takeover deal which suggests further consolidations in the industry.

In a statement, Esure Board said it was pleased to have reached an agreement with Bain Capital on the terms of a recommended cash offer.

As a result and under the terms of the proposed acquisition, each Esure shareholder will be entitled to receive 280p in cash for each Esure share held. This represents a premium of approximately 37% to the closing price per Esure share of 204 pence on 10 August 2018 (this being the last business day prior to the possible offer announcement released by Esure on 13 August 2018)

Chairman Sir Peter Wood, Esure largest shareholder, supported the Bain Capital deal and he is set to earn £371 million from it. Speaking to Reuters, Wood said “It is very good for all my colleagues, all the employees because Bain Capital are going to grow the business and invest heavily,”

He will remain Chairman of the group after the takeover and will reinvest £50 million.

Wood with a £150m investment from Halifax bank launched the online insurer Esure.com during the dot-com boom in 2001. After a management buy-out in 2010, the insurer became an independent company and listed as Esure Group Plc. in London in March 2013 at 290 pence per share.

The company provides insurance products to more than two million homeowners, drivers, holidaymakers, and pet owners across the UK.

Earlier, the insurer released its interim results for the first half year of 2018, which showed pre-tax profits falling 20% from £45.1m to £36.1m.

Darren Ogden, Interim Chief Executive Officer, said: “The first half of 2018 has seen continued growth in premiums and polices in a period impacted by exceptional weather costs … and these contributed to exceptional costs of £14m in the Home and Motor accounts.”

Luca Bassi, managing director of Bain Capital Europe, feels that Esure will grow positively, given its adept and focused way of working, and the way it puts technology to its best use. Insurance providers who operate from advanced technology says Bassi, are in the best position to drive customer satisfaction at competitive prices and that too, at a profit.

Insurance industry in troubles

However, the Esure 20% drop in profits this year is not unique among insurers. In fact, several of them have reported record losses due to an unusual spate of claims because of natural calamities and a series of regulatory updates and effects of Solvency II, the European Union (EU) initiative to introduce a solvency system better matched to the risks of insurers.

Few others are restructuring their operations by participating in mergers and acquisitions (M&A) with their non-performing or under-performing entities. In October 2017, Bermuda-based AXIS Capital acquired Novae Group in a £478 million ($615m), creating an insurer and reinsurer with $6 billion in gross written premium globally and $2 billion in London, making it a top ten insurer and reinsurer at Lloyd’s of London.

Earlier this year, giant French insurer AXA acquired the XL Group (aka XL Catlin), one of the leading global Property & Casualty commercial lines insurers and reinsurers in a £12 billion ($15.3bn) deal. Under the terms of the transaction, XL Group shareholders received £43.20 ($57.60) per share.

XL reported losses exceeding $1 billion for the 2017 third quarter, blaming natural catastrophe Hurricanes Harvey, Irma and Maria for the results. XL CEO, Mike McGavick revealed that the events had a “significant” impact on XL Group’s financial results for the quarter.

Moody’s, in a report, noted that the insured catastrophe losses in the third quarter of 2017 might turn out to be among the highest in the past two decades. Nonetheless, it added that insurers and reinsurers are sufficiently well capitalized to absorb the losses, albeit depleting their capital reserve.

Consolidations and InsurTech

Low interest rates, EU new regulatory updates such as the GDPR (General Data Protection Regulation), and natural catastrophe events are all contributing to the insurance business cycle downwards phase.

Many governments around the world introduced “Quantitative Easing” (Central banks increasing the money supply) and reduced the interest rates at record lows to fight off the 2008 recession. This affected insurers, who have struggled to make decent returns from the investments they must hold to cover potential claims.

Bermuda-based reinsurer Validus Holdings reported it made a net loss of $250 million for the third quarter of 2017, and further losses during the first quarter of 2018 – due partly to more expenses, an underwriting loss in its insurance segment and a drop in income in the reinsurance division.

American International Group (AIG) eager to re-establish its reputation and to re-enter the Lloyd’s of London insurance market recently finalised the acquisition of Validus Holdings in a $5.56 billion deal.

The adverse business insurance environment has proven difficult for some firms to generate enough money to invest in technology innovations or upgrades, and acquisitions on their own. Hence, the current dynamics suggest more consolidations to come.

If not consolidations then the remarkable insurance technology (InsurTech) trend has the potential to disrupt and worry many insurance players. InsurTech has seen a phenomenal growth and is already impacting insurers around the world.

By taking advantage of new technologies to provide coverage to more digitally savvy customer base, technology-led companies enter the insurance sector and proceed to steal the incumbents’ customers.

InsurTech is what Esure did during the dot-net boom; it used the then-nascent internet to streamline the process of buying car and home insurance, and passing on those savings to careful and responsible customers.

The Bain Capital investment offers Esure the opportunity to do it again, disrupting the insurance market.

Chairman Peter Wood said “As a private company and with Bain Capital’s backing, Esure will be able to invest behind the innovation required to fully realise the opportunities in this market. I am pleased to be continuing as Chairman and am fully aligned with Bain Capital, who I believe will be a tremendous partner in the next phase of Esure’s journey.”

Smartphones have become one of the greatest risks for auto insurers. Analysts blame mobile devices for a sharp increase in motor vehicle accidents in the United States.

America’s motor vehicle accident rate increased by 5% between 2011 and 2016, the National Council on Compensation Insurance (NCCI) calculated. The volume of workers’ compensation claims fell by 17.6% during the same period.

Smartphones are the likely cause, around 27% of US motor accidents involved phone use. Smartphone caused crashes are 12% more likely to involve a fatality, the NCCI claimed.

Vehicle accident risk is exploding

Disturbingly, those statistics might be an undercount. “There is strong evidence to support that underreporting of driver cell phone use in crashes is resulting in a substantial underestimation of the magnitude of the public safety threat,” the National Safety Council declared.

The frequency of auto accidents and the number of auto accident claims have increased since 2011. Not coincidently, the percentage of smartphone owners rose from 27% to 81% between 2016.

Financial risks to auto insurers are increasing because smartphone-related accidents cause more injuries. Auto accident claims are 80% to 100% higher than average compensation claims because of severe injuries.

Smartphones are increasing insurers’ costs

Vehicle accidents made up 28% of claims over $500,000 (£391,973), the NCCI discovered. In contrast, claims over $500,000 accounted for just 5% of all accidents.

American auto accidents are more expensive because the nation lacks National Health Insurance. Therefore, private insurers must cover all the medical costs of most accidents.

The fatality rate from auto accidents is 12 times greater than other accidents. Moreover, a vehicle accident is more likely to result in a costly death claim or lawsuit.

The NCCI expects the growing smartphone risk to increase the cost of insuring individuals in some professions. Accident risks for lorry drivers, cab drivers, salespeople, and delivery drivers increased because of smartphones.

The NCCI’s findings indicate that risks from vehicle accidents will increase for the foreseeable future. Disturbingly other data corroborates the NCCI’s findings.

Road traffic accidents have exploded worldwide in recent years, the Population Reference Bureau (PRB) calculated. Traffic accidents are now the leading cause of accidental death and a significant cause of ill-health.

Vehicle accidents cause 1.2 million deaths and 50 million injuries globally each year, the PRB estimated. Disturbingly, those figures will get far worse.

“And if present trends continue, road traffic injuries are predicted to be the third-leading contributor to the global burden of disease and injury by 2020,” the PRB warned. Unfortunately, the PRB did not include smartphones in its calculations.

Traffic fatalities in the United States increased by 5.6% between 2015 and 2016, the National High Traffic Safety Administration (NHTSA) discovered. Interestingly, the NHTSA blamed reckless behaviour, such as drunkenness, speeding, and lack of seat-belt use, rather than smartphones for the increase.

The number of distracted deaths decreased by 2.2% during 2016, NHTSA data indicates. Therefore, the smartphone danger might be exaggerated.

Future of traffic accident risk

Vehicle accident risks and costs to insurers will increase for the foreseeable future. Technologies like smartphones are magnifying the risks by increasing the distractions available to drivers.

Insurers will pay more traffic claims and those claims are likely to be greater in coming years. Consequently, many insurers will reduce their exposure to traffic accidents by exiting that business. Other insurers will trim risks by offering specialized auto insurance and leaving specific markets.

Higher-accident risks will be problematic for American auto insurers. The largest US vehicle insurers, such as GEICO, use a discount marketing model based on low rates. Increased risks might make such rates unprofitable.

The mitigation of smartphone risks will be difficult for insurers. Solutions like cell-phone blocking in vehicles will be unpopular and hard to implement. Enforcement of laws against texting and driving is difficult. Monitoring policyholders’ in-car phone usage would be difficult and potentially illegal.

Ironically, technology in the form of autonomous vehicles is the most promising solution. Unfortunately, widespread adoption of self-driving vehicle technology is probably several years off.

Therefore, insurers should expect dramatic increases in vehicle-claims and pay-outs for the foreseeable future. Auto insurance may no longer be the lucrative segment it once was.

United States’ central bank, the Federal Reserve System, has proposed a major change to its venerable credit-transfer service Fedwire.

The Fed wants to adopt the ISO 20022 Messaging format for the Fedwire Funds Transfer Service. A press release indicates that the Fed’s Board of Governors is taking comments on the proposed change right now.

The ISO 20022 is an international standard for financial messages designed to standardize and simplify the process. Adopting ISO 20022 would make it easier and cheaper for Fedwire customers to make transactions outside the United States.

One of the world’s oldest funds transfer systems

Fedwire, or the Federal Reserve Wire Network, is one of the world’s electronic-funds transfer systems. The Fedwire began as a telegraphic system back in 1915. Over the years the system was upgraded to Telex, and eventually to a computer network.

Today’s Fedwire Funds Service provides same-day transactions to government agencies, banks, and banks that have Federal Reserve Bank master accounts. Fedwire is used to settle commercial payments, settle positions between financial institutions, complete clearing arrangements, pay US federal taxes, and buy and sell federal funds.

Every Fedwire transaction is processed individually and settled immediately and finally upon receipt. The Fedwire depends upon a highly-secure electronic network that connects thousands of members. The Fedwire operates for 21.5 hours every business day (Monday through Friday). Funds are processed in Eastern Standard (New York) time.

The Fedwire is critical to America’s banking system because it ensures liquidity for banks, businesses, and government agencies. By having access to Fedwire, those institutions have continuous access to the Fed and money.

Fedwire joins the world

The Fedwire currently operates on a proprietary messaging standard that limits connectivity with institutions outside the United States.

Currently, institutions might have to join Fedwire to settle payments to, or receive funds from, the Fed. Adding ISO 20022 would give institutions all over the world the capability to settle Fedwire transactions on a same-day basis.

The ISO 20022 adoption would give foreign banks and financial institutions greater access to the American market. Fedwire is one of the two main large-volume payment systems operating in the United States.

This would increase business opportunities, but it would increase the exposure of American banks to troubles overseas. An unintended side effect of America’s adoption of ISO 20022 might be more exposure to liquidity crises at foreign banks.

If the Board of Governors approves it, the Fedwire would adopt ISO 20022 in three phases between 2020 and 2023. The Federal Reserve has been examining the possibility of utilizing ISO 20022 since 2012.

World’s central banks are increasing connectivity

The Fedwire ISO 20022 proposal is the latest effort to increase connectivity among the world’s financial institutions and central banks. Many of the efforts involve cryptocurrency and blockchain.

Leading the way is the People’s Bank of China (PBOC), which has set up a Digital Currency Research Lab. The Lab applied for 41 cryptocurrency and blockchain technologies in its first year of operation.

The PBOC’s governor Zhou Xiaochuan thinks a national digital currency is inevitable in China, The China Dailyreported. Despite that Zhou is not in a rush to adopt a digital coin, he apparently fears the effects cryptocurrency bubbles might have on the wider economy.

Consequently, the PBOC has attempted to ban private cryptocurrencies in China while researching an official one. Zhou confirmed reports that the PBOC has set up an institute to develop a national cryptocurrency.

The Federal Reserve is planning to issue a paper that will reveal its official position on cryptocurrency. Former Fed Governor Kevin Warsh has been promoting FedCoin a cryptocurrency issued by the Federal Reserve, according to The New York Times. It is not clear if Warsh’s proposal has official support.

Central bankers are interested in blockchain because that technology would theoretically allow the extension of same-day payment settlement systems like Fedwire to ordinary citizens. That would enable governments to distribute welfare benefits, pensions, basic income, or emergency funds directly to everybody.

Banks developing blockchain based settlement systems

There are some private efforts to develop a blockchain-settlement solution for central banks. These experiments include BABB (the Bank Account Based Blockchain) an Ethereum-based cryptocurrency and blockchain platform. BABB even bills itself as a blockchain solution for central banks.

A different approach is being tried by the Utility Settlement Coin (USC) and the Hyperledger Project. Both USC and Hyperledger are trying to develop blockchain-based settlement services that will directly connect major banks. The USC is being developed by a consortium that includes the Bank of New York-Mellon and UBS.

Hyperledger is backed by IBM and includes Deutsche Bank, Bank of New York Mellon, and HSBC. The banks are interested in the blockchain because it theoretically offers a far higher level of encryption and security than competing technologies.

Unfortunately, blockchain is much slower, and far less capacity than existing transfer systems. Existing blockchain technologies like Ethereum and Bitcoin can only process less than 20 transactions a second. The limited capacity of today’s blockchains would make it impossible to process the volume of settlements central banks require.

Despite the limitations, solutions like the blockchain and ISO 20022 have the potential to greatly increase connectivity between financial institutions. Insurers should pay attention because increased bank connectivity can increase risks to the financial system – such as the possibility of liquidity crises.

Amazon appears to be on the cusp of its long-anticipated entrance into the insurance industry – and markets appear nervous.

Shares in insurance companies wobbled in June following a report that the online retailer was considering adding home insurance. The insurance offering would be in combination of its connected home devices.

However, although this is a clear indication of where and how Amazon might enter the market, the company remains silent about its future plans leaving competitors to guess where its full effects might be felt.

Amazon has expanded well beyond its early iteration as an online alternative to brick-and-mortar book and music stores. Through Amazon.com and a range of other brands, the online retailer now accounts for 44% of online sales and 4% of all retail sales in the US.

The common element is that each brand or offering, even cloud computing AWS (Amazon Web Services) and streaming media, sticks to Amazon’s main intent.

“We strive to offer our customers the lowest prices possible through low everyday product pricing and shipping offers, and to improve our operating efficiencies so that we can continue to lower prices for our customers. We also provide easy-to-use functionality, fast and reliable fulfilment, and timely customer service.”From Amazon’s 2017 Annual Report

The question is, will financial and insurance products be the next set of items you can add to your cart?

Amazon Finance or Amazon Insurance?

As Amazon has grown, the potential for the company to expand even farther into areas such as finance and insurance has been an increasing concern. Alex Rampell, general partner at Andreessen Horowitz, described Amazon as the “most formidable” of the tech companies who might enter the sector.

So far, Amazon’s financial offerings differ little from other retailers, many of which offer store-branded credit cards, layaway plans or other forms of consumer credit.

Due to its role as a reseller or storefront for smaller brands, Amazon also has a small loans program, backed by Bank of America, which makes loans to small businesses who sell through the Amazon site.

These are relatively modest steps but Amazon may be quietly establishing a beachhead into the financial industry which could have extensive repercussions.

While Amazon quietly expands its financial offerings, insurance seems to be where the retailer is preparing for a much more active role. Several key developments over the last 18-24 months indicate that this effort is well underway.

First, the company introduced Amazon Protect, point of sale product insurance offered to consumers at check out. Amazon Protect launched in the UK and rolled out in selected European markets in 2016.

Amazon Protect explainer by Loop Films

Similar to its financial offerings, point of sale product insurance is a relatively standard retail practice, particularly where technology or white goods are concerned. Nevertheless, this was the company’s first foray into insurance and, for a firm adept at gathering and analysing consumer data, will no doubt have provided valuable insights into consumer behaviour.

The company’s second step towards becoming an insurance provider was Amazon’s partnership with US home construction firm Lennar. Under this arrangement, smart home devices provided by Amazon were placed into the developer’s model homes. Linked to Amazon’s Alexa AI system, these smart devices could control thermostats and lighting but also doorbells and alarm systems.

This addition of safety and security devices raised concerns that Amazon was going to use these as a springboard into home insurance.

Third, the company announced a partnership with JP Morgan and Berkshire Hathaway to tackle issues concerning the provision of healthcare in the US.

“JPMorgan Chase, along with our partners Amazon and Berkshire Hathaway, recently formed a joint venture that we hope will help improve the satisfaction of our healthcare services for our employees (that could be in terms of costs and outcomes) and possibly help inform public policy for the country. The effort will start very small, but there is much to do, and we are optimistic.”

Jamie Dimon, CEO JP Morgan in the company’s 2017 Letter to Shareholders

Ostensibly a move to improve delivery of healthcare to the three companies’ combined workforce of over 1 million staff, this partnership set off a wave of speculation that the initiative might become something much bigger.

Buffett, Bezos and Dimon have stressed that they are focussed on their own staff and even a million people is a tiny fraction of the hundreds of millions in the US who require health coverage. Nevertheless, this partnership added fuel to the fire of speculation surrounding Amazon’s ambitions.

Finally, the clearest sign of its intentions are the reports that Amazon is investing in InsurTech and aggressively hiring from that sector. Amazon invested $15.7 million in Indian InsurTech firm Acko in early 2018 as part of an agreement which positioned Amazon be the distributor for Acko’s insurance products in India.

Aggressive recruitment campaigns targeting InsurTech staff from firms like Lemonade are another indicator that the company is looking at ways to apply its existing technological and data advantage to the insurance sector.

Many advantages but significant challenges remain

With these signs that Amazon is firmly set on entry into the insurance sector, it is worth considering the pros and cons for the firm as it makes this move.

Firstly, the company enjoys high levels of customer satisfaction and trust. While this is a core value of the firm, achieving consistently high ratings is difficult. As Jeff Bezos himself puts it, the company faces “divinely discontent” customers.

“Their expectations are never static – they go up…People have a voracious appetite for a better way, and yesterday’s ‘wow’ quickly becomes today’s ‘ordinary’.”Jeff Bezos, Amazon’s Letter to Shareholders 2018.

However, unlike dissatisfaction with a faulty toaster, a poor experience buying an insurance policy, and more importantly problems making a claim, will have much wider repercussions. Maintaining such high levels of satisfaction with something as complex as insurance will be challenging.

Secondly, Amazon collects “a mountain of data…to build up a “360-degree view” of you as an individual customer”, data which should help actuarial calculations and consumer targeting. Triggering an offer to add a child to your life insurance policy when you order onesies for a new-born is in many ways no different to suggesting that you also buy diapers and formula.

This ability to seamlessly add insurance products to other transactions is the third and possibly greatest of Amazon’s advantages.

A key differentiator for Amazon compared to other firms is that consumers already have financial relationship with Amazon. Contrast this to Google or Facebook. Both firms hold immense amounts of consumer data, probably more than Amazon, and despite people’s grumbling about privacy, these services remain popular with users. However, it is businesses which have transactional relationships with Google and Facebook whereas everyone with an Amazon account will have at least considered making a purchase on the site.

So, while social media firms may hold more data and be more visible to consumers, it is Amazon’s transactional relationship that gives it a clear advantage when it comes to making sales.

Finally, Amazon is a technology company and one willing to tackle complex technical challenges such as web-services and streaming entertainment. While the practical challenges of providing insurance will be significant, the company has already solved many of the technical issues associated with serving an enormous customer base online. Adding InsurTech expertise to this foundation gives the firm a real competitive advantage.

This is not to say that everything will be plain sailing for the firm, despite these strengths.

Insurance is a very different product from DVDs, books and electronics so customers may still experience some dissonance if auto insurance pops up as a recommended buy. Moreover, insurance by its very nature adds exposure to the company increasing both financial and reputational risks. Finally, Amazon will have to tackle the issue of approvals and licensing from the countries and states where it wants to offer insurance.

At times, Amazon has had a contentious relationship with several states and its hometown of Seattle. However, unlike skirmishes over corporate taxes, Amazon will have less heft with local authorities if it seeks approval as an insurer. Anyone slighted previously, or those worried about local ‘mom-and-pop’ insurers, may be less inclined to approve Amazon’s application.

Even with these headwinds, Amazon’s sheer size, customer loyalty and technical know-how will make it a daunting player in the financial and insurance sectors. Its entry to both markets has been careful and discreet but the repercussions are likely to be significant and, in the case of insurance, may be felt sooner rather than later.

Germany’s biggest bank, Deutsche Bank has shifted an important part of its euro clearing business to Frankfurt from London due to Brexit. The move is unlikely to affect jobs – the work still exists – the bank will only be doing it differently.

Earlier this year, the bank had announced its intention to slash over 7,000 roles in cost-cutting efforts, but evidently, this has not happened yet.

The change, as reported to the Financial Times (FT) by a company spokesman, is being seen as a victory in the Deutsche Bank’s attempt to get a more significant share of the euro clearing market. It is currently dominated by the London Stock Exchange.

Following the Brexit vote, contenders such as the Eurex Clearing, part of Deutsche Börse Group, have been making attempts to steal London’s crown. French finance minister Bruno Le Maire had previously suggested that Brexit could provide eurozone member states a means to gain control of the clearing business.

The fight against London’s financial sector supremacy has always been an ongoing battle. A serious blow occurred when it lost dominance in the trading of German government bonds to the Frankfurt-based Deutsche Terminboerse (DTB), Eurex’s ancestor.

Using technology, innovation and close cooperation between different parties within the sector, Eurex is now the second biggest euro clearing house and holds a market share of roughly 8 percent.

Hubertus Väth, managing director of consultancy group Frankfurt Main Finance, told FT that moving euro clearing to Frankfurt was “…on top of our priority list from the very first day after the Brexit referendum.”

What is euro clearing?

Clearing can be viewed as the “plumbing’ of financial services. In this process, a third-party performs the function of a middleman between a buyer and a seller for financial contracts, where there is an underlying value attached to a share, index, currency or bond.

The role of the clearing house is to provide a central point of access to facilitate simpler and swifter transactions. There is also a percentage of risk, as the clearinghouse bears the cost if a single side of the transaction does not pay up.

As a kind of compensation for bearing that risk, buyers and sellers deposit the money in a dedicated account with the clearing house. The system is designed to reduce the domino-effect in the event of a debt default affecting the entire system. UK clearing houses have a considerable chunk of the market in euros.

Miles Celic, the chief executive of financial services lobby group TheCityUK, tells Sky’s Ian King about euro clearing and its significance in London.

The UK accommodates both the biggest Over-The-Counter (OTC) Euro foreign exchange transactions market and OTC interest rate derivatives market, worldwide. Dealings to the tune of about 1 trillion euros occur in the UK on a daily basis, a considerably larger volume as compared with the 395 billion euros that are dealt with daily in the United States.

Clearing is considered to be an essential ingredient for financial stability. However, Deutsche Bank feels that the fallout of Brexit is threatening this financial stability. It could due to material risks likely to develop in the derivatives market after Brexit. This was pointed out by the Bank of England earlier this year.

Deutsche Bank shifts focus to Europe

The basic mantra of Deutsche Bank seems to a shift of focus from the UK and the world to Europe, in a bid to facilitate reforms that have been long since overdue. New Deutsch Bank CEO, Christian Sewing is impatient to get started, stating, “There’s no time to lose!”

Sewing’s predecessor, John Cryan first initiated Deutsche Bank’s clean-up operation over the last three years. However, Cryan had burdens with a legacy of long-pending issues which bogged him down and prevented him from implementing significant reforms within the organisation.

He was more like a demolition man trying to break up large chunks of the organisation into manageable parts. Now, Christian Sewing has the herculean task of rebuilding the bank from those various fragmented sections.

The new strategy according to Sewing, is to reinforce the bank’s European and German customer base and pull out of areas which have proven to be costlier and riskier. Sewing said that the bank is committed to its international investment banking operations. There is a need to “concentrate on what we truly do well,” he said.

Supporting the Deutsche Bank move, German finance minister, Olaf Scholz in a recent statement stated: “To minimise risk for financial stability, it is indispensable that [the clearing of euro-derivatives] is subject to strong regulation and supervision in full conformity with EU standards.”

Rebuilding lost confidence

There is a similar occurrence taking place in the United States. However, in this case, the context is slightly different. Deutsche Bank, in its attempt to get a slice of the pie along with its US competitors, neglected its domestic private customers and later, even its local corporate customers.

This negligence resulted in an exodus of local Deutsche Bank customers to other banks. Big German companies started going to other banks for financing their mergers and acquisitions, and the bank lost much business due to this unwarranted arrogance on its part.

Now, in a bid to repair the damage caused to its domestic customers, Deutsche Bank wants to focus more on the domestic market, projecting “commitment instead of arrogance.” Although according to Christian Sewing there will be no withdrawal from US business, experts feel that it will eventually happen, but perhaps in instalments.

Experts have compared the presence of Deutsche Bank in the US to Volkswagen’s business operations in that country. Just like the way Volkswagen’s business has declined to a negligible level in the recent years, they feel that Deutsche Bank will perhaps be likely to travel along the same road, maybe finally maintaining a nominal presence there.

The writing on the wall

With the onset of Brexit and recent developments in Deutsche Bank, it becomes apparent that the organisation is going to be conducting business in a very different way in the days to come. It seems that several changes and restructuring of the bank will take place under the new leadership of Christian Sewing.

Like several other banking organisations who have undergone downsizing and streamlining their financial operations, Deutsche Bank has seen the writing on the wall. One lives in times where business is valued if it is profitable; or else, it’s not a business worth having.

Deutsche Bank’s move out of the UK can be interpreted as a step in the right direction, provided that the new leadership can make intelligent decisions according to the changing times.

The Chartered Insurance Institute (CII) has launched a Public Trust Index that provides the industry with much needed insight into key measures of consumers’ confidence. In order to improve customers’ satisfaction, insurers require a better understanding of the opinions of insurance buyers.

The survey comprised of in-depth interviews with industry regulators and public bodies, in addition to consumers and SMEs (Small Medium Enterprises), supports the industry shift from a structural focus on the premiums to developing customer relationships through value and trust.

Accordingly, confidence in insurers was the leading priority whereas premiums were a low priority. Confidence in insurers is followed by easy buying process (70%) and good protection from the insurance product (68%).

The Index has also revealed gaps in areas of importance to consumers and their perception of industry performance in these areas. The performance gap is largest for rewarding customer loyalty at 13% followed by an easy buying process and good protection from the insurance product with 7% gap, respectively.

The industry challenge is to improve trust by closing these gaps between consumers’ expectations and industry performance. The biggest hurdle is addressing the lack of perceived loyalty. The large performance gap reflects consumer discontent with the practice of insurers charging new customers lower prices but raising the renewal price for existing customers, known as dual pricing.

Dual pricing under the spotlight

Under the current controversial practice of dual pricing, customers pay a higher price in return for loyalty to insurance providers. Since new customers are offered more attractive pricing to sign up for new insurance products, long-term customers pay more for their insurance – in effect, subsidizing the discounted pricing.

This pricing regime sends faulty market signals by penalizing insurance buyers in the form of higher prices for long-term customer loyalty.

“If competition is working well in a market, it should not overly disadvantage existing customers over new customers,” states the Financial Conduct Authority (FCA) Business Plan 2018/2019, which has made tackling dual pricing a priority.

Since April 2017, the FCA has sought to ensure fairer pricing by requiring insurers to list the previous year’s premium alongside renewal offers.

While consumers are lowering their premiums by shopping around, prices are still far from being equalized. Consumers can get better pricing by taking their insurance business elsewhere.

In the second year of a home insurance policy with the same insurance provider, a consumer can save £45 on a home insurance policy by switching providers, according to Consumer Intelligence. In the ninth year, the savings jumps to £124.

Broker relationship matters most

Small and medium businesses value, before all, the broker advisor relationship. As with consumers, however, this trust has been breached by the practice of employing dual pricing.

The prospect of subsidizing the insurance of competitors is an even more contentious issue in the business insurance market. To the contrary, SMEs seeking to reduce business expenses expect insurers to offer a higher value proposition through loyalty discounts, for example, as well as policy extras and no claims bonuses.

Furthermore, small businesses value protection at reasonable costs, claims processing facilitated with ease and speed, and complaints handled efficiently.

Overall, the survey found that the claims process boosted confidence for insurers. Most consumers reported satisfaction with a claims process that was handled quickly (74%), respectfully (70%) and with the control of the policyholder in the process (68%).

Policyholders’ loyalty, however, can easily be betrayed on a technicality. Such was the anguishing case of a homeowner who lost his five-bedroom house in a fire as recounted by James Daley upon receiving the CII Consumer Champion Award.

In his speech, Daley tells how the insurance company rejected the homeowner’s claim when his house burnt down. “The house had 5 bedrooms – and 2 attic rooms which had not been completed according to buildings regulations. When the house burned down, the insurer told the customer that his house had 7, not 5 bedrooms, and because they didn’t cover 7 bedroom properties, they wouldn’t pay a penny of his claim. Worse still, the Ombudsman agreed.”

Social media has become a critically important channel for customer service and feedback. A bad insurance claim story like this can go viral and can jeopardize the insurer and the whole industry’s reputation.

One way for the insurance industry to address its reputational issues, concludes the report, is to step up to the challenge of becoming partners in risk management with its customers. As a provider of risk management solutions beyond insurance, the industry will be incentivized to create more value for customers through innovative risk management products.